Introduction

U.S. cannabis M&A is not “business as usual.” Federal illegality still shapes everything: tax (IRC §280E), banking access, diligence depth, and how much of a deal can actually close on schedule (licenses, ownership approvals, local permits).

As of February 26, 2026, the federal government has signaled movement but has not delivered full federal legalization. The Department of Justice initiated a formal rulemaking process in May 2024 to move marijuana from Schedule I to Schedule III, which (by statute) requires formal “on the record” rulemaking and an opportunity for a hearing. A December 18, 2025 White House executive order directed the Attorney General to complete that rescheduling rulemaking “in the most expeditious manner” consistent with federal law, but an executive order does not itself change the Controlled Substances Act schedules.

Investor readiness in cannabis is mostly about removing avoidable risk: clean ownership and cap table, provable compliance, defensible tax positions (especially COGS/280E), and a bankable control environment for cash, inventory, and excise taxes. IRS guidance and litigation history make clear that documentation and accounting methods are not optional.

In plant-touching deals, deal structure is often dictated by license transfer rules and regulator timing more than by tax optimization. In representative states, change-of-ownership approvals can be pre-approval requirements and may trigger new applications at certain thresholds.

Valuation in U.S. cannabis is heavily shaped by (a) regulatory friction, (b) cost of capital, and (c) 280E-driven EBITDA distortion—so buyers often anchor on unit economics and cash generation after excise taxes and compliance cost, using structures like earnouts/clawbacks, seller notes, and equity-heavy consideration to bridge uncertainty.

Regulatory landscape and what changed through early 2026

Federal vs. state remains the core tension. Under federal law, marijuana remains illegal to “manufacture, distribute, or dispense” absent federal authorization, which is why federal-bank compliance and federal-tax rules continue to bite even when state operations are fully licensed.

Federal scheduling and rescheduling process

In May 2024, the Department of Justice submitted and published a proposed rule to transfer marijuana from Schedule I to Schedule III, explicitly noting the Controlled Substances Act requires formal rulemaking “after opportunity for a hearing.” The same proposal is reflected in the official Federal Register publication (May 21, 2024).

On December 18, 2025, Donald Trump issued an executive order titled “Increasing Medical Marijuana and Cannabidiol Research,” which references the pending Schedule III rulemaking and directs the Attorney General to complete it expeditiously in accordance with federal law.

Why founders and CFOs should care: IRC §280E applies only to Schedule I or II controlled substances. If marijuana is actually moved to Schedule III with an effective date, 280E’s federal disallowance should no longer apply going forward based on the text of the statute (subject to IRS implementation details, transition issues, and unresolved edge cases).

DOJ enforcement guidance and banking implications

Federal enforcement posture has shifted over time through DOJ memoranda. The 2013 James M. Cole memo articulated federal enforcement priorities that, in practice, influenced how banks and investors assessed risk. The 2018 memo by Jefferson B. Sessions rescinded prior DOJ marijuana-specific guidance.

For banking, the critical reality is: the 2014 Financial Crimes Enforcement Network guidance remains a baseline framework for depository institutions that choose to serve marijuana-related businesses, including customer due diligence expectations and ongoing suspicious activity reporting (SAR) mechanics. This is one reason cannabis operators still face constrained access to large banks even amid rescheduling signals and executive branch support.

As of late January 2026, industry reporting indicates Congress has not enacted a comprehensive federal safe-harbor banking statute for cannabis (SAFE/SAFER).

State licensing and transferability is usually “change of ownership,” not a free transfer

State license mechanics can force structure. Representative examples:

- California: California regulations require reporting/supplying information when owners change (including submitting required information for new owners within a stated window).

- Oregon: Oregon Liquor and Cannabis Commission change materials state that certain changes must be approved before changes are made and that a change of ownership of 51% or more requires a new application.

- Massachusetts: Massachusetts Cannabis Control Commission publishes a dedicated Change of Ownership or Control request form tied to its regulations.

- Illinois: Illinois Department of Financial and Professional Regulation provides change-of-ownership guidance for adult-use licenses, including a stated fee per ownership change/transfer and illustrative examples of multi-step transfers.

- Colorado: Colorado’s marijuana rules include a defined process for a “Change of Controlling Beneficial Owner,” with statutory/regulatory basis and application requirements embedded in rule text.

Deal takeaway: “We bought the company” is not the same as “we can operate tomorrow.” Licensing approvals, local permits, and “control person” background checks can become gating items that dictate close date and escrow timing.

Deal types and structuring choices

In U.S. cannabis, structure is mostly a balancing act among: (1) license continuity, (2) liability isolation, (3) tax outcomes (including 280E), and (4) financing constraints tied to banking and securities market access.

| Structure | What transfers | Why buyers use it | Why sellers resist it | Cannabis-specific watchouts |

|---|---|---|---|---|

| Asset purchase | Selected assets + assumed liabilities | Strong liability ring-fencing; purchase price allocation and step-up potential | Licenses/contracts may not be assignable; seller may retain “bad” liabilities | License/permit assignment may be prohibited or require re-application; inventory transfer often regulated; landlord consent hurdles. |

| Equity (stock / membership interest) purchase | Entity (and its licenses) stays intact; ownership changes | Often best for license continuity; contracts stay in place | Buyer inherits all historical liabilities (tax, compliance, HR) | “Change of ownership/control” approvals can be required pre-close; disclosures of beneficial owners; local endorsements. |

| Merger (parent/sub or statutory merger) | Combination into surviving entity | Can simplify multi-entity rollups; can be used for consideration flexibility | Complexity; dissent rights; regulatory steps | Same licensing/ownership approval issues as equity; integration risk is higher. |

| Roll-up / platform consolidation | Series of acquisitions into a “platformco” | Builds scale; purchasing power; brand and distribution leverage | Control dilution; earnout disputes | State-by-state fragmentation makes synergy models fragile; compliance integration is hard. |

| Sale-leaseback (real estate) tied to M&A | Real estate sold; ops continue under lease | Non-dilutive liquidity; can finance expansion or acquisition | Long-term rent burden | Regulatory/local approvals for premises changes; lender/landlord compliance diligence. |

| SPAC / de-SPAC (rare for plant-touching U.S. ops) | Public listing via SPAC business combination | Faster access to public capital (in theory) | High disclosure and liability; performance scrutiny | SEC’s 2024 SPAC rules increased required disclosures and aligned certain liabilities closer to traditional IPO dynamics; projections and de-SPAC disclosures face tighter standards. |

How to choose: a practical decision framework

Most founder/CFO teams should start with three questions:

- Will the target license stay valid after closing? If the state treats “control changes” as requiring pre-approval—or a fresh application above a threshold—this can force a staged closing or a longer outside date.

- Are historical tax and compliance risks containable? If not, an asset deal or heavy indemnity/escrow structure may be the only way to price risk without killing the deal.

- Can you finance the structure? Financing often wants collateral. If the “real value” is a license that cannot be pledged or transferred freely, lenders will price higher, tighten covenants, or require additional security.

Valuation, metrics, and financial modeling

Core valuation methods used in cannabis deals

In practice, sophisticated buyers triangulate:

Comparable companies (public comps): Useful for directional EV/Revenue and EV/EBITDA, but distorted by market microstructure, listing constraints, and 280E’s impact on “clean” EBITDA. Public MSO valuation snapshots (example: median EV/2026 EBITDA and EV/2026 revenue for a defined MSO cohort) are published by industry tracking services like Viridian and are often used as an external reasonableness check.

Precedent transactions (deal comps): Most valuable when the target’s state, license type, and asset package match yours (stores, cultivation canopy, manufacturing throughput, brands, distribution). A key nuance: many disclosed precedent multiples are on “Adjusted EBITDA,” which may not reflect cash taxes under 280E.

Discounted cash flow (DCF): The right tool for multi-asset operators—if your model correctly reflects excise taxes, compliance costs, capex for facilities, working capital needs for inventory, and assumed cost of capital.

Unit economics / license economics: Particularly for retail-heavy operators: revenue per store, gross margin after product & perishables, labor model, loyalty economics, and the cost to maintain compliance.

Multiples observed: a practical benchmark table

This table blends (a) disclosed plant-touching transaction multiples from issuer press releases/filings and (b) public market valuation snapshots as context. Use it to sanity-check—not to price your company.

| Sub-sector | Observed / referenced multiple (examples) | What drives the range in cannabis |

|---|---|---|

| Plant-touching multi-state / multi-asset acquisitions | ~4.175x 2024 “Closing/Reference EBITDA” was cited across multiple acquisitions announced/closed by Vireo Growth Inc. (e.g., Proper, WholesomeCo, Deep Roots) with clawback mechanics tied to later EBITDA outcomes. | State mix, license scarcity, near-term capex needs, and whether EBITDA is “real” after 280E and excise taxes. |

| Plant-touching retail/cultivation tuck-ins | Example disclosure: acquisition described by The Cannabist Company (then Columbia Care) cited ~3.4x estimated revenue and ~4.7x estimated adjusted EBITDA for a California acquisition announcement. | Local market competition, store productivity, wholesale pricing pressure, and regulatory friction (local permits, delivery rules). |

| Public MSO valuation snapshot | Example: a Viridian valuation tracker page cited median EV/2026 EBITDA and EV/2026 revenues for a defined MSO cohort (market cap threshold), roughly ~5–6x EV/EBITDA and ~1–2x EV/Revenue in that snapshot. | Public market liquidity, governance, dilution overhang, debt maturities, and federal reform optionality. |

| Banking/legal reform “option value” | Not a multiple; it’s a scenario driver. Rescheduling rulemaking progress is a valuation catalyst because it can change tax economics (280E scope depends on Schedule I/II language) but does not itself create full banking safe harbor. | Markets price probability and timing. CFOs should model multiple “effective dates” and transition periods, not a single outcome. |

Cannabis-specific modeling adjustments finance teams should standardize

Normalize EBITDA for cannabis reality. Create at least two EBITDA layers:

- EBITDA (GAAP / book)

- Adjusted EBITDA (with transparent add-backs)

- “Cash EBITDA after excise & compliance” (your internal truth metric)

Then quantify “280E distortion” explicitly: the delta between taxable income under 280E constraints and taxable income under normal deductibility. The reason is statutory: 280E disallows deductions/credits for Schedule I/II trafficking, leaving COGS as the key allowable reduction from gross receipts.

Illustrative pro forma example (hypothetical)

Assume a buyer acquires a single-state operator with 6 dispensaries + 1 cultivation site.

- Purchase price: $60.0M

- Structure: $15.0M cash at close + $25.0M seller note + $20.0M earnout (2-year)

- Base year revenue: $48.0M

- Base year Adjusted EBITDA: $12.0M

- Working capital peg: $2.5M, with true-up at close

- Escrow: 10% of upfront consideration for 18 months (reps + tax/compliance)

A finance team should produce, at minimum, these pro forma views:

- Pro forma P&L (with synergy build + integration costs)

- Pro forma cash flow (with debt service, excise tax payments, capex, and inventory build)

- Pro forma leverage (Net Debt / EBITDA variants)

- Pro forma ownership and dilution (if equity is used)

Financing structures and investor landscape

Capital structure tools most common in cannabis M&A

Equity (common / preferred / convertible): Often used because debt is expensive and because equity aligns sellers (especially in roll-ups). Equity-heavy consideration is visible in announced/closed M&A transactions where consideration is paid in shares.

Senior secured debt: Available, but underwriting is conservative due to federal illegality and collateral complexity. Even as executive actions signal rescheduling, large banks still cite legal ambiguity and risk.

Seller notes / seller financing: Common bridge when bank debt is limited or when buyer wants to reduce cash close.

Earnouts / clawbacks: Extremely common as a pricing bridge because regulatory approvals, market pricing, and license constraints create wide outcome uncertainty. The Vireo transactions provide clear examples of disclosed clawback provisions tied to later EBITDA performance milestones.

Revenue-based financing (RBF): Often structured as a share of revenue until a cap is returned; used when EBITDA is volatile but revenues are observable and controllable through POS and seed-to-sale reporting.

Key investor types and how they behave in cannabis

Strategics (operators / brands / distribution / technology):

They underwrite operational synergies: procurement, cultivation utilization, wholesale channels, shared services, and licensing footprint. Their diligence is intense on compliance integration because one weak node can threaten licenses across the brand family.

Private equity:

Traditional PE often prefers businesses that can be diligence-clean, financeable, and scalable without federal illegality risk bleeding into the fund’s broader banking and LP relationships. In cannabis, PE structures may be more creative (holdco structures, non-plant-touching adjacencies, or minority investments with protective rights) because of banking and exit constraints.

Family offices:

Often more patient and can underwrite regulatory risk if they believe they have informational advantage or relationships in a state market. They still demand proof of compliance and clean tax.

Cannabis-focused funds:

They tend to move faster, understand licensing nuances, and accept cannabis-specific deal mechanics (earnouts, escrow for tax exposures, inventory verification). Their biggest pain point remains reliable banking rails and exit optionality.

Model cap table example (hypothetical)

Assume you raise $20M to fund acquisitions.

| Security | Pre-money Shares | New Shares | Post-money Shares | % Ownership (Post) |

|---|---|---|---|---|

| Founders (common) | 7,000,000 | — | 7,000,000 | 46.7% |

| Employee option pool (unallocated) | 1,000,000 | — | 1,000,000 | 6.7% |

| Seed investors (preferred) | 4,000,000 | — | 4,000,000 | 26.7% |

| Series A investors (new) | — | 3,000,000 | 3,000,000 | 20.0% |

| Total | 12,000,000 | 3,000,000 | 15,000,000 | 100% |

Investor readiness means you can produce this (and a fully diluted version) in minutes, not days—tied to signed docs, not memory.

Due diligence, tax, banking, and compliance playbooks

This is where cannabis deals are won or die. Buyers pay less (or walk) when diligence reveals: undocumented ownership changes, weak inventory controls, non-defensible 280E positions, or licensing exposure that cannot be fixed inside the deal timeline.

Due diligence checklist table

Use this as a working checklist. Build a data room that mirrors it.

| Workstream | “Green flag” deliverables | Common cannabis “red flags” |

|---|---|---|

| Financial | Monthly close package (12–24 months), reconciliations (cash, inventory, A/R), POS-to-GL tie-outs, same-store metrics, capex schedule | “Spreadsheet accounting,” missing bank recs, income that can’t be traced to POS, inventory shrink that’s unexplained |

| Tax (federal + state) | Filed returns + workpapers, 280E/COGS methodology memo, excise filings, nexus analysis, uncertain tax position schedule | Aggressive COGS capitalization not supported by method; incomplete excise tax filings; unresolved audits |

| 280E/COGS mechanics | Documented inventory accounting method; clear distinction between COGS (return of capital) vs disallowed deductions; controllable chart of accounts | IRS has emphasized inventory costing rules and methods where 280E applies; weak documentation creates audit exposure. |

| Licensing & compliance | License certificates, renewal history, notices of violation, SOPs, seed-to-sale reconciliation, ownership/control disclosures filed with regulators | Ownership/control changes not properly noticed/approved; local permit mismatch; compliance violations with unresolved corrective action plans. |

| Banking & cash controls | Bank account list, armored car contracts, cash count SOPs, dual control logs, AML/KYC documentation for key counterparties | Account instability; commingling; unexplained cash variances; inability to maintain banking relationships due to compliance gaps |

| Supply chain | Vendor contracts, COAs/testing records, recall SOP, packaging/label approvals | Untraceable batches; inconsistent COAs; vendor noncompliance that can become your liability post-close |

| IP & brand | Trademarks (where possible), licensing agreements, brand style guides, domain ownership, product formulations | Brand not owned by the licensee entity; key IP held by a founder personally; licensing revenue not documented |

| Real estate & environmental | Leases, estoppels, zoning letters, environmental reports (Phase I where appropriate), security plan | Lease prohibits cannabis or has weak assignment rights; zoning nonconformity; unresolved environmental issues |

| HR & labor | Employee roster, wage compliance, benefits, handbook, key employment agreements, LUT/union or labor peace items where applicable | Misclassification; high turnover; “key person” risk; missing documentation required by state/local rules |

| Litigation & claims | Docket summary, demand letters, product liability claims, consumer complaints | Undisclosed disputes; pattern of product complaints; legacy partner claims |

The cannabis tax core: IRC §280E and IRS positions

What 280E says: No deduction or credit is allowed for amounts paid/incurred in a trade or business that “consists of trafficking in controlled substances” in Schedule I or II that is prohibited by federal or state law.

What that means operationally: Your tax team must treat COGS and inventory accounting as a first-order strategic issue. IRS internal guidance (Chief Counsel IRS memo) has addressed how taxpayers trafficking in Schedule I/II substances determine COGS under §471 and has pushed back on using additional capitalization rules to convert nondeductible expenses into inventoriable costs beyond what was permitted when 280E was enacted.

Litigation backdrop matters: Federal appellate decisions have upheld denial of deductions under 280E and rejected attempts to expand inventory cost inclusion beyond permissible bounds in related disputes.

State tax nuances: not all states follow 280E the same way

State treatment varies. Examples from representative states:

- Colorado: State materials describe a “Marijuana Business Expense Deduction” allowing licensed marijuana businesses to deduct business expenses disallowed for federal purposes under 280E when computing Colorado taxable income (with statutory citations).

- Oregon: Oregon statute addresses expenses of marijuana-related trade or business with specific references to how 280E applies and state-authorized conduct exceptions; Oregon Department of Revenue instructions also reference ORS 317.363 and treatment for expenses otherwise barred by IRC §280E.

- California: The California Franchise Tax Board’s cannabis guidance states that licensed cannabis businesses may deduct COGS and all ordinary and necessary business expenses for California purposes, while unlicensed cannabis businesses may not deduct other business expenses (referencing 280E for more detail).

Investor readiness asks for: (1) your state-by-state tax posture memo, (2) “licensed vs. unlicensed” proof chains where relevant, and (3) a consistent treatment of excise taxes in your financial reporting.

Banking and payments constraints

The 2014 FinCEN marijuana banking guidance describes how financial institutions can offer services consistent with Bank Secrecy Act obligations, including specific customer due diligence steps (license verification, reviewing licensing applications, monitoring for red flags) and ongoing SAR filing expectations. FinCEN publications have reiterated that the SAR structure in that guidance remains in place until changed.

Practical impact for operators: account onboarding and continuity depend on your ability to produce clean compliance artifacts quickly—licenses, ownership, source-of-funds transparency, and consistent reporting—because the bank’s burden is structural, not optional.

Negotiation, closing mechanics, and post-close integration

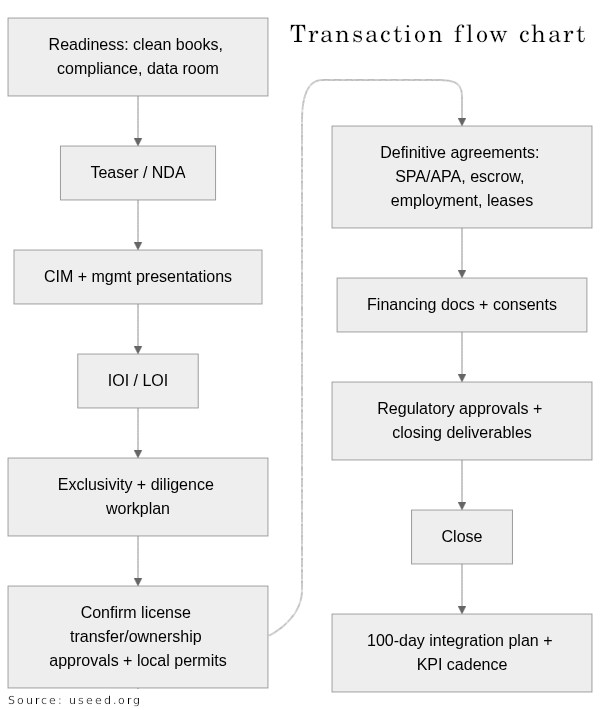

Transaction flow chart

Key term sheet concepts (practical template)

Below is a usable LOI/term sheet skeleton. Treat it as a checklist, not legal advice.

1) Parties / structure

- Buyer entity, seller entity, target entities, licensed entities

- Deal form: asset / equity / merger

- Included/excluded licenses, premises, brands, IP

2) Purchase price

- Enterprise value

- Cash at close / equity / seller note / earnout

- Working capital peg + true-up mechanics

- Treatment of cash, debt, transaction expenses

3) Regulatory approvals

- Required filings for change of ownership/control

- Timing assumptions; cooperation covenants

- Outside date + extension rights; drop-dead provisions

4) Representations & warranties

- Financial statements

- Compliance, licensing, seed-to-sale, testing/labeling

- Taxes (280E methods, excise filings, audits)

- Title to assets; IP ownership; litigation

5) Indemnities and survival

- Caps/baskets

- Special indemnities: tax, licensing, product liability, employment

- Survival periods

6) Escrow / holdback

- % of consideration

- Release schedule

- Claims process

7) Earnout/clawback (if any)

- Metric definition (revenue, EBITDA, gross profit, store count)

- Control of operations during earnout

- Audit rights and dispute resolution

8) Covenants

- Ordinary course operations

- No leakage; capex/opex limits

- Hiring/firing limits on key staff

- Compliance covenants

9) Exclusivity + confidentiality

- Exclusivity period

- Break fee or expense reimbursement (if any)

10) Closing conditions

- Financing

- Regulatory approvals

- Third-party consents (leases, key vendors, MSAs)

- Bring-down and material adverse effect (MAE)

Escrow, holdbacks, indemnities: cannabis-specific emphasis

Cannabis deals tend to push more value into risk-managed buckets because unknowns are real:

- Tax escrows (280E method risk, excise, payroll tax exposure)

- Licensing/compliance escrows (open violations, unresolved ownership disclosures)

- Inventory valuation adjustments (especially cultivation/manufacturing)

Even when parties use “market” escrow percentages, cannabis buyers often demand longer survival periods for tax and licensing representations because (a) regulator discovery can be delayed and (b) tax audits can land years later.

Sample timeline and milestones table

Assume “state unspecified,” and you are operating in representative states where change-of-ownership approvals may be required.

| Week | Milestones | CFO/finance deliverables | Key gating risks |

|---|---|---|---|

| 0–2 | Readiness sprint | QoE-style close package, tax posture memo, entity chart, data room index | Missing cap table/ownership clarity; weak reconciliations |

| 3–4 | NDA, teaser, CIM, first meetings | KPI pack (store-level), compliance summary, normalized EBITDA bridge | Overstated EBITDA; incomplete excise treatment |

| 5–6 | LOI signed; exclusivity starts | Draft sources/uses, working capital schedule, lender packet | Buyer financing constraints, valuation gap |

| 7–10 | Diligence deep dive | Weekly diligence tracker; tax workpapers; inventory support | Compliance gaps; licensing approval timeline uncertainty |

| 11–14 | Definitive docs negotiated | Closing checklist; estimated close balance sheet; pro formas | Lease consents; regulator conditions; earnout disputes |

| 15–20+ | Regulatory approval window (varies by state) | Cash runway plan; integration budget | Delays on change of ownership/control approvals |

| Close + 0–4 | Close + Day-1 control transition | New bank/cash SOPs; inventory controls; KPI dashboard | System cutover risk; cash handling failures |

| Close + 5–14 | 100-day integration | Monthly KPI cadence; synergy realization reporting | Culture/HR turnover; compliance drift |

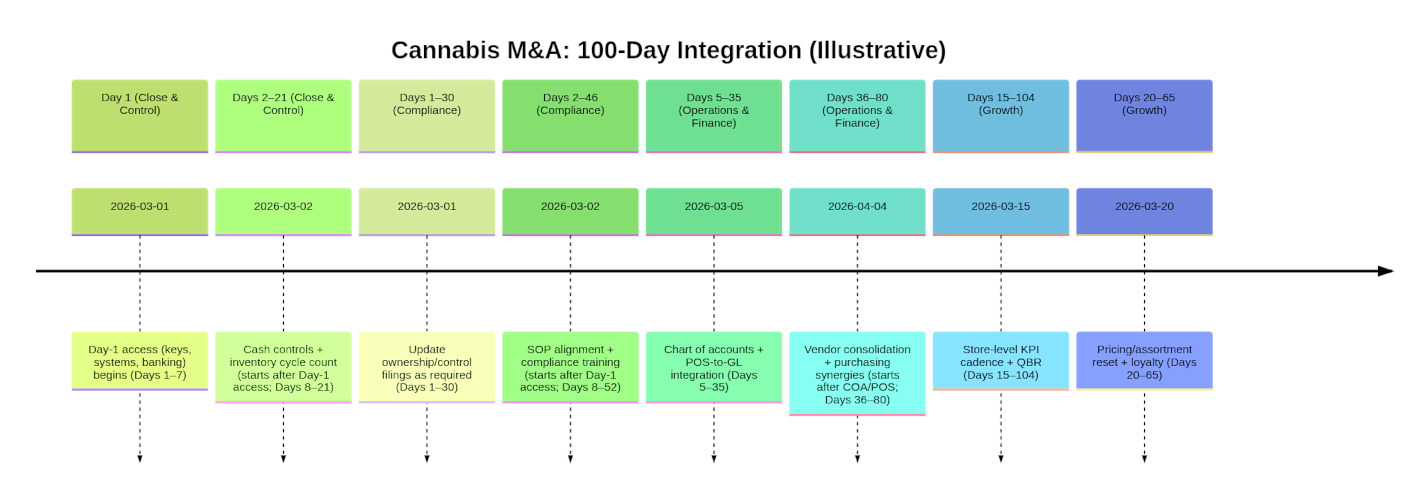

Integration timeline chart

Post-close KPIs that sophisticated buyers expect

Focus on a small set that ties to value creation and risk control:

- Revenue quality: same-store sales, basket size, loyalty retention, promo intensity

- Gross margin integrity: gross margin by category; wholesale vs retail mix; shrink; write-downs

- Inventory discipline: seed-to-sale reconciliation exceptions; turns; days on hand; obsolescence

- Compliance health: violations, corrective actions, training completion, audit findings

- Cash conversion: cash taxes paid, excise timing, working capital, capex vs plan

- Synergy scorecard: headcount efficiencies, vendor savings, facility utilization, procurement pricing

Common pitfalls and mitigation (high-frequency issues)

Pitfall: mis-modeled tax burden. Teams use “normal” EBITDA multiples without explicitly modeling 280E cash tax drag, then find the target cannot service debt. Ground your model in the statute and your documented COGS method; assume audit scrutiny.

Pitfall: assuming licenses “transfer.” In many states, what you can do is apply for and obtain approval for changes in ownership/control, sometimes triggering new applications at thresholds. Build a regulatory critical path early and draft deal terms around it (outside date, covenants, staged closing).

Pitfall: weak cash/inventory controls. Cannabis is inventory- and cash-heavy; diligence will test whether POS, seed-to-sale, and GL reconcile. Fix this before you go to market.

Pitfall: bank fragility. FinCEN’s framework forces banks to do ongoing monitoring; a compliance miss can cause account closure at the worst time (during diligence or post-close transition). Treat banking readiness as a compliance deliverable.

Pitfall: term sheet ambiguity on earnouts. In cannabis, earnouts are common because uncertainty is structural; define metrics precisely, define control rights, and define dispute mechanics.