Introduction

AI and automation in cannabis cultivation are no longer future tech, as they’ve become the operating system for cost-competitive producers, especially in indoor and greenhouse environments where labor, energy, and compliance overhead dominate the P&L.

Market pricing pressure is the forcing function. On March 20, 2026, Cannabis Benchmarks reported the United States wholesale cannabis spot index at $1,002 per pound (with weekly volatility). In that context, small improvements like single-digit yield gains, a few points of energy reduction, or shaving weeks of labor hours can be the difference between positive cash flow and distress.

The technology stack is converging around five layers: (1) sensors and equipment telemetry, (2) automated climate/irrigation control, (3) computer vision and phenotyping, (4) predictive analytics for yield/quality/maintenance, and (5) compliance-grade traceability (seed-to-sale) plus audit-ready data integrity. The financial reality is that post-harvest automation (bucking/trimming) often has the fastest payback, while AI “autopilot” climate or irrigation layers require solid data infrastructure and disciplined change management to translate algorithms into harvest-weight results.

Regulation is both a tailwind and a constraint. Many jurisdictions require serialized tracking and frequent inventory reconciliation, which increases the value of integrated software and clean data pipelines. At the same time, privacy and cybersecurity risks rise as cultivation becomes more digitized and camera-rich.

A final macro variable: in the U.S., the The White House issued an executive order on December 18, 2025 aimed at accelerating cannabis rescheduling; however, multiple analyses emphasize that rescheduling requires a formal administrative process and—until a final rule takes effect—federal constraints remain. This uncertainty matters for financing costs, expansion planning, and the attainable ROI horizon for automation CAPEX.

Disclaimer: This post is not investment advice.

Current technologies in use across the cultivation value chain

Cultivation automation is best understood as a closed-loop system: sensors observe biology and environment; controllers actuate HVAC, lighting, irrigation, and CO₂; analytics forecast outcomes; and operators enforce the decisions inside operational constraints. The Resource Innovation Institute frames this plainly: designing, installing, commissioning, and operating automation and control systems efficiently “requires specialized expertise,” even if basic manual operation feels intuitive.

Computer vision is the fastest-moving layer. Vision systems typically combine fixed cameras, mobile/trolley cameras, and plant-level segmentation models to quantify growth rate, canopy uniformity, stress signatures, and labor quality (e.g., pruning/defoliation consistency). In parallel, academic work continues to show that imaging (including hyperspectral) can quantify plant nutritional status and stress non-destructively, including in cannabis/hemp contexts.

Predictive analytics is where finance meets agronomy. In practice, “predictive” means: yield and harvest timing forecasts tied to sales commitments; anomaly detection (e.g., irrigation valve drift, VPD instability); and predictive maintenance for climate equipment. Industry deployments increasingly emphasize forecast reliability because revenue timing and wholesale pricing are extremely sensitive to supply swings.

Environmental controls and crop steering are the operational foundation. This includes room-level or greenhouse-level control of temperature, humidity, dew point/VPD, CO₂ dosing, and lighting schedules, plus irrigation “steering” strategies that intentionally manage substrate water content (drybacks) to influence plant generative vs vegetative behavior. The key point for investors: the controller is not the moat; the moat is the data + disciplined standard operating procedures (SOPs) that make the controller repeatable across rooms and sites.

Robotics is more common in post-harvest than in the grow room. Today’s most proven “robotics” in cannabis is mechanization: conveyors, buckers/debudding machines, trimmers, sorting lines, and automated packaging interfaces. This reflects tough physical constraints in flowering rooms (dense canopies, variable plant morphology, contamination control), versus the high ROI of mechanizing repetitive post-harvest labor.

Seed-to-sale tracking and traceability remain mandatory infrastructure in many regulated markets. Track-and-trace systems create chain-of-custody records and often require tagging at plant and package levels, with transfers and adjustments logged within prescribed timelines.

Leading vendors and case studies

The vendor landscape splits into five clusters: (1) climate and irrigation controllers, (2) AI overlays and analytics platforms, (3) vision/phenotyping, (4) traceability platforms, and (5) post-harvest mechanization. The table below emphasizes documented features and cited outcomes; pricing is included only where public list prices exist (many enterprise deployments are quote-based).

| Vendor (cluster) | Representative products / capabilities | Deployment signal & documented outcomes | Public pricing anchors (where available) |

|---|---|---|---|

| Addium (irrigation AI) | “Intelligent irrigation” positioned as AI decision-making that executes irrigation without fixed schedules/setpoints; tooling for dryback calculations and crop steering workflows. | Vendor positions this as automation for crop steering and operational efficiency; outcome claims are largely qualitative in public materials. | Enterprise pricing typically quote-based (no durable public list price). |

| Growlink (fertigation/controls) | Automation for irrigation recipes and feeding, with a value proposition around reducing mixing errors and input waste; wireless monitoring marketed as reducing wiring friction. | Public case studies are limited in hard metrics; positioning is strong on labor/input savings, especially where frequent recipe changes occur. | Quote-based for larger systems; pricing varies by site complexity. |

| TrolMaster (room controllers) | Hydro-X Pro is a room controller with touchscreen UI; published specs include capacity limits (e.g., up to 50 sensors and 50 device stations) for modular expansion. | Common in multi-room indoor builds as a standardized controller layer; ROI depends on commissioning quality and sensor calibration discipline. | Public retail pricing exists (~$2.5k USD, varying by region and distributor). |

| Priva (enterprise greenhouse control) | Priva positions its gateway/data layer as cloud-connected (including Microsoft Azure) and oriented to connecting grower-level data with decision support, with dedicated API resources for integration. | Increasing integration with AI forecasting platforms is a theme (yield forecasting positioned as reducing “big swings” and volume risk). | Quote-based; economics depend on scope (control hardware + integration + support). |

| Hoogendoorn Growth Management (enterprise greenhouse control) | IIVO “Intelligent Algorithms” are marketed as using weather forecasts, historical learning, and proactive management to steer greenhouse climate. | Integration maturity varies by legacy stack; some legacy environments require workaround integration approaches rather than clean APIs (see interoperability case discussion below). | Quote-based; often deployed at large greenhouse scale. |

| Koidra (AI control overlay) | KoPilot is an AI automation overlay that can sit on top of existing greenhouse controllers and operate within safety boundaries set by operators. | Case study (non-cannabis greenhouse) reported +6.8% yield, −4.84% steam energy, and +12.23% “overall energy efficiency improvement” across a six-month period (results context-specific). | Quote-based; ROI hinges on integration effort and baseline variability. |

| IUNU (vision + analytics) | LUNA described as combining fixed and mobile cameras with environmental sensors to measure and record crop conditions; marketed toward inventory control, crop growth monitoring, labor, and predictive maintenance use cases. | A case study in leafy greens reported +14% grams per plant and elimination of prior 2% crop loss after using crop images to adjust irrigation strategy. | Funding datapoint: company announced a $20M round (Series B extension) led by S2G Investments (2025), supporting expansion of AI-driven greenhouse tech. |

| Gardin (phenotyping) | Optical sensing positioned around photosynthesis/plant stress indices; public materials describe integration into climate platforms (e.g., displayed via Priva One) to connect plant response with climate execution. | Best fit is high-value greenhouse operations and R&D/phenotyping use cases; ROI depends on whether insights translate into stable SOP changes. | Quote-based; often sold into enterprise greenhouse tech stacks. |

| Metrc (traceability) | Track-and-trace platform selected by many jurisdictions; California’s official FAQ describes RFID-based unique identifier tags (plant/package), “confirm receipt” workflows, and the ability to connect third-party applications through API/file upload. | Example of regulatory adoption: Illinois’ official cannabis tracking page identifies METRC as the state’s inventory tracking system. | In California, the official FAQ states tag cost is included in the license fee (no additional charge), though this varies by jurisdiction. |

| BioTrack (traceability) | Marketed as compliance and “track-and-trace” tooling for regulated cannabis, with portals and system resources oriented to jurisdictional deployments. | Value is primarily compliance risk reduction and process standardization; economics depend on jurisdiction requirements and integration complexity. | |

| CenturionPro Solutions (post-harvest mechanization) | Published performance: models marketed with throughput in wet/dry pounds per hour and “human trimmer replacement” claims (e.g., Original up to 10 lbs dry/hour; TableTop up to 4 lbs dry/hour; Original marketed as replacing up to 60 workers). | Public list price example: Original Standard System listed at $4,995 USD on the manufacturer site. | $4,995 USD (Original Standard System). |

| Twister Trimmer (post-harvest mechanization) | Published throughput for T4 configurations includes wet trimming capacities (e.g., multiple configurations with stated lbs/hour). | Widely sold through commercial distributors; ROI depends on whether the operator’s target quality spec tolerates machine finish vs hand finish. | Example listing price: ~$12,187 USD (T4, retailer listing; varies). |

| Mobius Trimmer (bucking + lines) | MBX Bucker marketed at $23,900 on the vendor shop; listings describe “strip 150 lbs of flower per hour” and integrated stem chipping for waste reduction. | Public “hand-trimming cost” narratives exist in vendor materials; treat as directional inputs for modeling, not as audited benchmarks. | $23,900 USD (MBX Bucker, vendor shop). |

| Trym (ops/MES-lite) | Cannabis cultivation operations software; published case study: a Massachusetts operator reported ~23 labor hours saved per week versus whiteboards (time saved across managers and staff). | Financing datapoint: company disclosed a $3.1M seed round (2020) to advance cultivation software. | SaaS pricing typically subscription-based; specifics often quote-based. |

Case study takeaway: the most repeatable “hard outcome” evidence in public sources tends to be (a) mechanization throughput and replacement claims for post-harvest machines and (b) controlled-environment greenhouse case studies that quantify yield and energy deltas under AI overlay. Cannabis-specific AI yield case studies exist but are often gated behind marketing forms or not published with enough methodological detail to underwrite them like a capex memo.

Economics, CAPEX/OPEX ranges, and ROI scenarios

This section separates (1) anchored numbers backed by public sources and (2) assumptions used to build financial scenarios where vendors do not publish consistent price sheets.

Operational facts from sources:

- Labor-intensive trimming is measurable. In the 2021 survey report, the median expected output per hand trimmer was 2 pounds per shift, and the average shift length was 7.3 hours.

- Machine trimming and bucking adoption is already mainstream (50% trimming machines; 19% bucking machines in that same survey).

- A representative wholesale price anchor exists in public, frequently updated reporting: $1,002/lb (U.S. spot index, March 20, 2026).

- Public list prices exist for some mechanization: e.g., CenturionPro Original $4,995; Twister T4 around $12,187 (retailer listing); Mobius MBX Bucker $23,900 (vendor shop). Sources cited in the table above.

- Yield/energy deltas under AI overlay can be quantified in at least some greenhouse deployments (6.8% yield increase and 4.84% steam reduction reported in one KoPilot case study).

CAPEX and OPEX ranges

The table below is intentionally order-of-magnitude, because many enterprise vendors quote per project. Where public prices exist, they are cited as anchors.

| Component | Typical scope in a commercial facility | Public price anchors | Practical range used in models (stated assumption when not public) |

|---|---|---|---|

| Room controller (HVAC/irrigation coordination) | 1 per room/zone, plus sensors and controlled relays | Hydro-X Pro retail examples around ~$2.5k USD. | ~$2k–$10k per room (controller + sensors + install). Assumption informed by retail controller pricing and typical commissioning effort. |

| AI overlay / closed-loop control (greenhouse) | Overlay on existing climate computer; requires data pipeline, integration, and safety constraints | Quantified case results exist; price usually quote-based. | ~$100k–$500k+ per site for integration + first-year deployment (assumption; depends heavily on legacy system integration). |

| Computer vision (plant-level monitoring) | Cameras + compute + analytics; often subscription-based | Descriptions of camera/sensor systems + public funding indicates enterprise scale; pricing typically quote-based. | ~$50k–$300k setup plus ~$20k–$150k/year subscription (assumption; depends on coverage density and features). |

| Post-harvest trimming (mid-scale) | 1–n trimmers depending on harvest cadence | CenturionPro Original $4,995 (vendor). | ~$5k–$25k per trimmer line for small-to-mid operations; $50k–$300k+ for industrial lines (ranges based on publicly listed models; model selection drives scale). |

| Bucking / debudding | Often paired with trimming to reduce upstream labor | Mobius MBX Bucker $23,900 (vendor shop) and 150 lbs/hour claim (listing). | ~$15k–$60k for commercial bucking; higher with conveyors/line integration (assumption anchored by listed prices). |

| Seed-to-sale / traceability integration | Required in many legal markets; includes workflows, training, and integration | CA: RFID UID tagging workflows and API support described in official FAQ. | $10k–$150k+ implementation (process + integration), plus ongoing compliance labor; software cost varies by jurisdiction and stack (assumption; driven by integration complexity). |

ROI scenario calculations

These are finance model scenarios: they explicitly separate cited input values from modeling assumptions. The payoff profile is highly nonlinear: ROI is dominated by (a) harvest volume cadence, (b) the price environment, and (c) whether the operation can operationalize the tech (commissioning + SOPs), not merely install it.

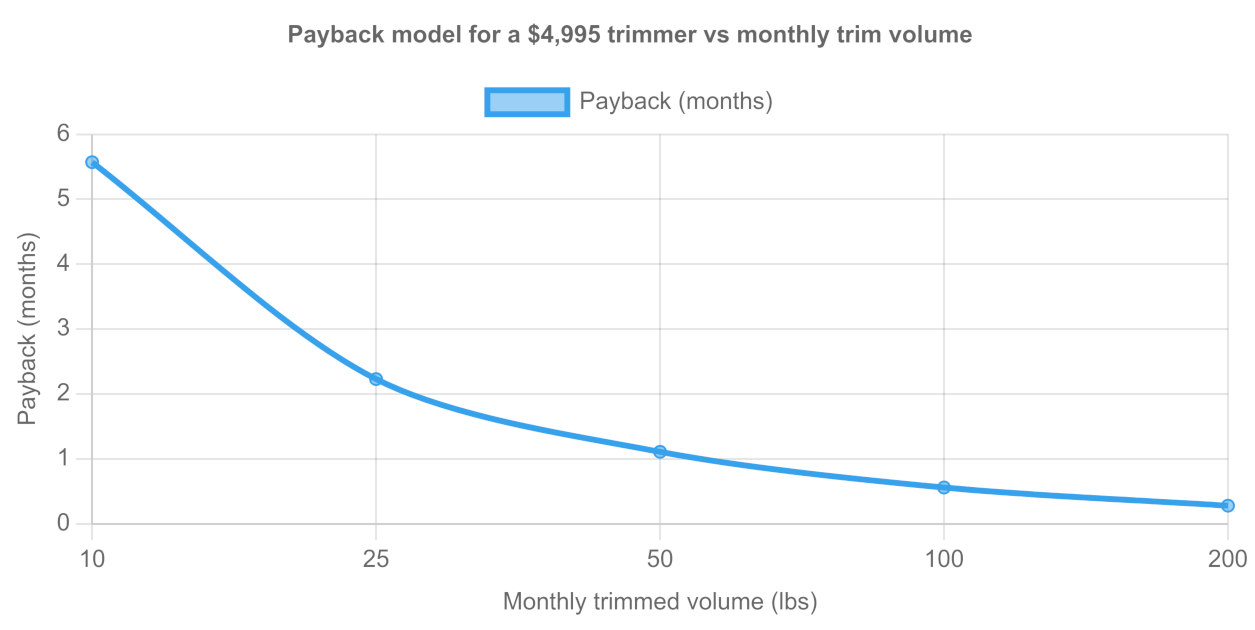

Scenario A: post-harvest trimming pays back quickly at modest volume

Inputs

- Hand trimming productivity: median 2 lbs/shift; shift length 7.3 hours.

- Trimmer CAPEX anchor: CenturionPro Original $4,995.

Assumptions

- Loaded labor cost: $26/hour (= $20/hr wage used in an industry case narrative + 30% payroll burden).

- Effective machine output: 5 lbs of dry product per hour (assumes ~50% utilization vs. rated capacity to reflect feeding, QA, stoppages).

Modeled result

- At 50 lbs/month of dry flower requiring final trim, modeled labor savings are about $4.5k/month, implying ~1.1 months payback on a $4,995 trimmer (before maintenance/consumables).

- At 10 lbs/month, modeled payback is ~5.6 months.

Quality caveat: a cultivation operator quoted in a trade publication reported up to a 7% increase in flower-to-trim ratio (cultivar-dependent) when switching from machine to hand trimming—suggesting machine trim ROI should be evaluated against the product’s target tier and remediation/rework costs, not only labor hours.

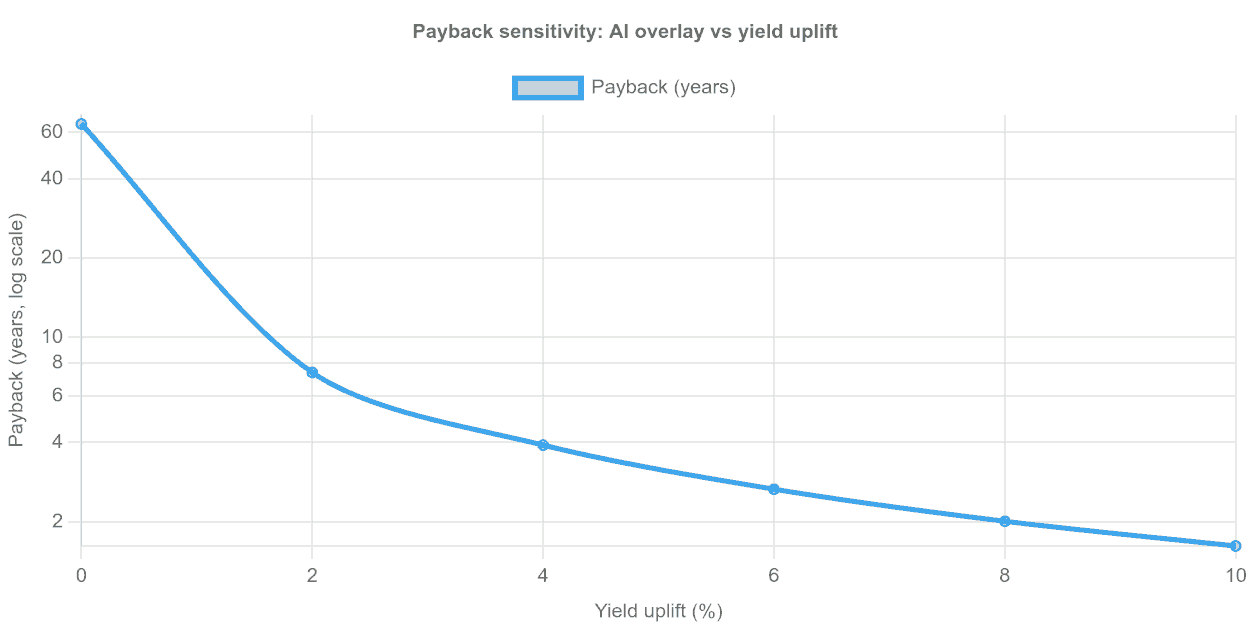

Scenario B: AI climate overlay ROI is dominated by yield uplift and integration cost

Inputs

- KoPilot case study reported +6.8% yield and −4.84% steam energy (context: greenhouse deployment).

- Wholesale price anchor: $1,002/lb (March 20, 2026)

Assumptions

- Facility output: 2,000 lbs/year of sellable flower (annualized).

- Contribution margin on incremental yield: 60% (variable costs assumed 40%; margin varies widely by region, product tier, and compliance cost).

- Annual energy spend: $250k; apply 4.84% savings to approximate cash savings from steam reduction (energy mixes vary heavily).

- Implementation economics: $200k CAPEX, $40k/year incremental OPEX (software/support).

- Labor/process savings from digitization: $31k/year (directionally anchored by a software case study; scaled to loaded cost).

Modeled payback sensitivity

- 2% yield uplift → ~7.4 years payback

- 6% yield uplift → ~2.7 years payback

- 10% yield uplift → ~1.6 years payback

This chart is intentionally conservative at low yield uplift because integration and subscription costs can overwhelm benefits unless the operation is large enough (or the solution materially reduces variability and crop loss). Interoperability and data plumbing are often underestimated cost centers in AI-centric projects.

Regulatory, compliance, and data integrity impacts

Traceability rules significantly shape cultivation automation because they force standardized data capture and increase the penalties for messy inventory practices. In California, the California Department of Food and Agriculture describes the CCTT–METRC system as mandatory for annual/provisional licensees and explains that RFID UID tags are ordered/assigned within the system, must be confirmed received before use, and track cannabis through transfers in the commercial supply chain. The same official FAQ notes that the system allows third-party application connections via standard API/file upload and that licensees are responsible for data entered by employees/contractors.

In Illinois, the state’s cannabis program page identifies METRC as the inventory tracking system, reinforcing the broader reality that many markets standardize on a state-selected platform rather than letting operators choose freely.

In Canada, Health Canada publishes a Good Production Practices guide that repeatedly ties GPP compliance to record-keeping requirements under the Cannabis Regulations (Part 11 references) and provides operational expectations that are difficult to meet reliably without controlled documentation and audit-ready systems.

For medical cannabis operators supplying pharmaceutical channels, the compliance bar rises further. The European Commission hosts EudraLex Volume 4 GMP guidance, and the European Medicines Agency maintains GMP/GDP Q&A resources—together reflecting that GMP environments expect documented processes, controlled records, and deviation management (which pushes operations toward validated software, access controls, and audit trails).

In the U.S., U.S. Food and Drug Administration has issued Data Integrity and Compliance With Drug CGMP guidance clarifying regulators’ expectations around data integrity for drug manufacturing systems, which is an important reference point for cannabis businesses that aspire to GMP-like operating credibility for medical markets.

Privacy and surveillance risk grows with cameras, biometrics, and cloud dashboards. The European Union’s GDPR (Regulation (EU) 2016/679) is the baseline reference for personal data processing obligations (lawful basis, minimization, security of processing, breach notification structures). In the U.S., state privacy laws increasingly affect cannabis operators that collect consumer data via loyalty programs or delivery platforms; California’s Attorney General explains that the CCPA grants consumers rights over personal information collected by businesses (a meaningful constraint if cultivation data systems connect directly to consumer identity data via vertical integration).

Macro-regulatory uncertainty also impacts automation underwriting. The White House executive order (Dec 18, 2025) aims to accelerate rescheduling, but reporting and legal analysis underline that rescheduling requires a formal rulemaking process and does not automatically make “flower products” federally compliant without additional regulatory steps. The tax angle is straightforward in statute: 26 U.S.C. § 280E disallows deductions for businesses trafficking in Schedule I or II controlled substances, which is why rescheduling off Schedule I/II is widely viewed as a potential margin catalyst—if and when it becomes final.

Operational challenges, integration risks, and cybersecurity

The hidden risk in cultivation automation is not “does the algorithm work?” but “can the facility execute stable inputs and integrate outputs into SOPs?”

Interoperability is commonly the critical path. A greenhouse AI deployment report described building an end-to-end IoT data infrastructure that had to interact with modern sensors and a legacy Hoogendoorn iSii control system; because the legacy system lacked a programmatic API, the project used Robotic Process Automation and Optical Character Recognition to interface and adjust setpoints. It explicitly notes that early assumptions about available APIs proved costly in engineering effort. This pattern is directly transferable to cannabis: many facilities are “Frankenstacks” of lighting controls, HVAC controllers, fertigation skids, and compliance platforms purchased in phases.

Data quality is the second failure mode. If temperature/RH/CO₂ sensors drift, or irrigation flow meters are miscalibrated, “AI optimization” becomes automated error. That is why third-party guidance emphasizes commissioning and specialized expertise rather than treating controls as plug-and-play.

Cybersecurity moves from IT to operational risk. Cultivation facilities increasingly resemble industrial control environments (remote monitoring, actuators, vendor cloud access). The National Institute of Standards and Technology CSF 2.0 lays out a practical risk taxonomy (Govern, Identify, Protect, Detect, Respond, Recover) that can be mapped onto cultivation OT/IoT stacks.

Meanwhile, International Society of Automation describes ISA/IEC 62443 as a lifecycle framework for securing industrial automation and control systems—useful when specifying segmentation, vendor remote access, and patch governance for greenhouse/indoor control networks. Real-world cannabis-adjacent breaches and vendor incidents reinforce that consumer and operational data exposure can become material (legal liability, license risk, and reputational damage).

Market outlook and investment thesis

The near-term outlook is shaped by three realities: price compression, energy intensity, and regulatory fragmentation.

Wholesale pricing remains volatile. Cannabis Benchmarks’ March 20, 2026 report placed the U.S. spot index at $1,002/lb, with state-level and grow-type swings described week to week. Volatility increases the value of reliable forecasting and production planning (to avoid “harvest gluts” that force distress sales), which is a core pitch for AI yield forecasting integrations.

Energy costs are structurally high indoors. An IEEE open-access energy modeling paper for indoor cannabis emphasized that HVAC (including dehumidification) and lighting dominate electricity consumption in typical indoor operations, referencing a 51% HVAC and 38% lighting split; it also computes an example electricity intensity of 1.24 kWh/sq.ft/day for a 4,000 sq.ft flowering canopy facility in its validation case.

A policy brief on cannabis energy use notes that energy efficiency regulation is challenging partly because cannabis remains federally illegal in the U.S., which limits federal code guidance and pushes states into bespoke approaches. This is a long runway for automation providers that can tie control decisions to measurable kWh/gram reductions.

Capital markets are gradually validating “picks-and-shovels” cannabis tech, but deal flow is uneven and often tied to broader controlled-environment agriculture rather than cannabis alone. Examples of disclosed financings: IUNU announced a $20M round led by S2G Investments in 2025; Source.ag announced a $17.5M Series B in 2025 to scale applied AI for controlled environment agriculture; and Koidra disclosed a $4.5M seed round (2022). Cannabis-specific software funding exists but is typically smaller; Trym disclosed a $3.1M seed round (2020).

On the consolidation side, MJBizDaily reported a notable valuation compression datapoint: Akerna sold its cannabis software businesses for $5 million in cash (2023), highlighting how quickly compliance software can de-rate when growth expectations reset or platform adoption shifts.

Investment thesis:

- Most durable value accrues to platforms that reduce unit cost and variance (less yield swing, fewer compliance errors), not just average yield. Forecast reliability reduces “volume risk,” which in turn reduces pricing risk and supports contracts.

- Interoperability is the moat. Systems that integrate cleanly across controllers, sensors, and traceability reduce the “hidden tax” of custom engineering (RPA/OCR-style workarounds).

- Post-harvest mechanization is the quickest underwriting win (fast payback, hard throughput).

- Regulatory uncertainty remains a discount factor in the U.S. Even if rescheduling advances, the process is formal and timing-sensitive; underwriters should treat tax relief and banking reform as upside scenarios, not base-case guarantees.

Practical recommendations for cultivators and investors

This section is designed to be used like an implementation memo: roadmap, KPIs, and procurement diligence.

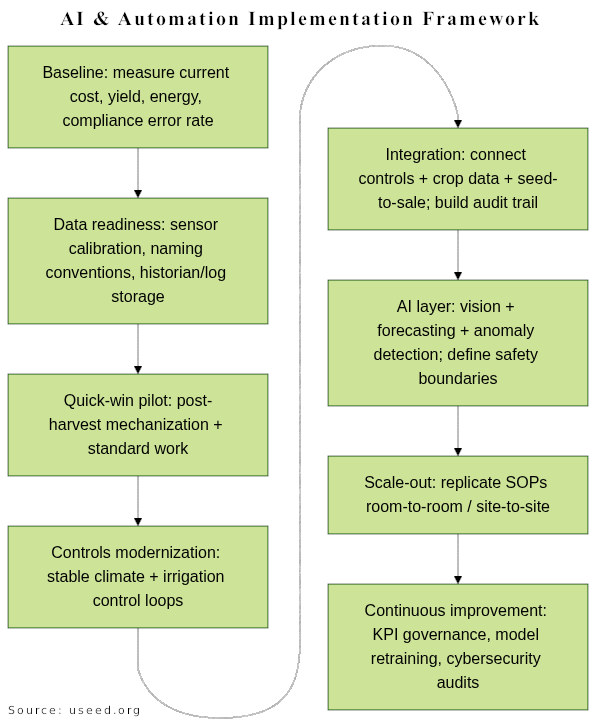

Implementation roadmap

Implementation roadmap

The sequencing matters because many AI projects fail on “plumbing” and change management rather than model accuracy. The reported need to build around missing APIs (RPA/OCR) is a reminder to budget integration as a first-class workstream.

KPIs that tie directly to ROI

A small set of metrics that map cleanly to margin and risk:

- Labor efficiency: labor hours per pound trimmed (or per pound packaged); overtime hours during harvest week (ties directly to mechanization ROI).

- Yield and uniformity: sellable pounds per sq.ft of canopy per cycle; coefficient of variation across rooms (variance is often more costly than mean shortfall).

- Energy intensity: kWh per pound (or kWh per gram), and HVAC vs lighting contribution where submetering exists (ties to control optimization and energy codes).

- Compliance integrity: number of inventory adjustments, frequency of late entries, and reconciliation time per reporting period (ties to seed-to-sale and license risk).

- Quality outcomes: flower-to-trim ratio and rework rate (ties to the “hand vs machine trim” trade-off).

Procurement checklist

Keep diligence practical and evidence-based:

- Integration proof, not promises: request live demos of API/file workflows and data export; verify how the vendor handles third-party integration (especially for track-and-trace connections).

- Commissioning plan: insist on a documented commissioning process (sensor calibration, alarm thresholds, fail-safes) and named responsibility for “who owns the numbers.”

- Safety boundaries and override logic: for AI control overlays, require explicit constraint logic and human override procedures.

- Cybersecurity baseline: map vendor controls to NIST CSF functions; for OT environments, require segmentation, access control, logging, and vendor remote access governance aligned with industrial cybersecurity practices (ISA/IEC 62443 framing).

- Evidence hierarchy: prioritize (a) published case studies with quantified outcomes, then (b) reference customers with comparable scale, then (c) marketing claims. Example: treat “human trimmer replacement” as a throughput proxy, not as guaranteed headcount reduction.

- Regulatory fit: validate that workflows match your jurisdiction’s tagging, reporting timelines, and audit expectations (and that responsibilities are clearly assigned).

For investors, the underwriting shortcut is to ask one hard question: “Can this operator replicate results across rooms and sites?” If the answer depends on a single head grower’s intuition rather than on controlled data, applied automation, and enforceable SOPs, the technology stack will not compound—no matter how impressive the demo looks.