Introduction

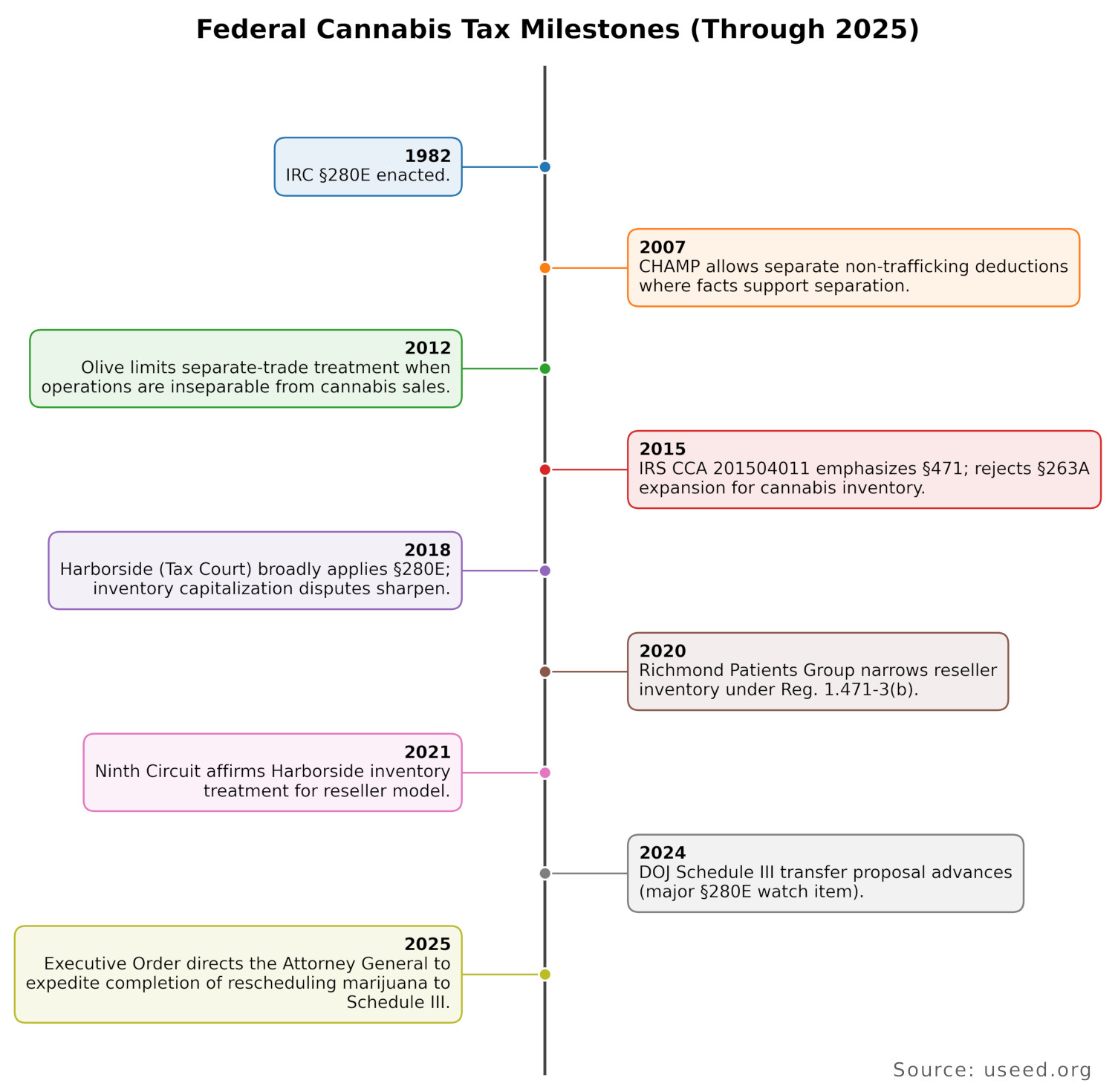

Federal cannabis taxation is still dominated by IRC §280E, which denies deductions and credits for amounts paid or incurred in a trade or business that “consists of trafficking” in a Schedule I or II controlled substance prohibited by federal law (and by the law of the state where conducted). This applies even if the business is state-licensed. The practical result for “plant-touching” operators is that taxable income is often close to gross profit, not net profit, and effective tax rates can be unusually high.

The center of gravity for planning and compliance is therefore:

- COGS (cost of goods sold) and inventory under §471 and related regulations, and

- Maintaining clean segmentation (where real) between trafficking and non-trafficking lines of business, because courts look hard at whether activities are genuinely separate trades or businesses.

At the state level, the U.S. cannabis tax burden is usually a stack: cannabis-specific excise taxes (often retail % or weight/potency-based), general sales taxes (in many states), local option cannabis taxes, and licensing/application fees.

State income taxation can be materially better than federal taxation in states that decouple from §280E for state income tax purposes (meaning they allow deductions the IRS disallows), but this varies and should be confirmed state-by-state.

For tax year 2025, several rate changes matter operationally:

- California: excise moved from 15% to 19% (July 1–Sep 30, 2025), then back to 15% (Oct 1, 2025 onward).

- Minnesota: cannabis gross receipts tax increased to 15% effective July 1, 2025 (and sales tax/local sales taxes also apply).

- New Mexico: cannabis excise increased from 12% to 13% starting July 1, 2025, with scheduled annual 1% increases thereafter toward 18% by 2030.

Near-term legal risk and opportunity in 2025 continued to center on: (a) how far taxpayers can push inventory capitalization without crossing into disallowed deductions, and (b) whether federal scheduling changes could remove cannabis from the §280E trigger (because §280E only references Schedule I and II).

A DOJ proposal to move marijuana from Schedule I to Schedule III was published in 2024 (comment period through July 2024), while more recently, the President signed an executive order in December for rescheduling, making this a major “watch item” affecting forward planning.

Federal tax framework for cannabis businesses in 2025

The rule you build everything around: IRC §280E

What §280E does. Section 280E denies any deduction or credit for amounts paid or incurred in carrying on a trade or business if that trade or business (or its activities) consists of trafficking in Schedule I or II controlled substances prohibited by federal law (or the relevant state’s law).

What §280E does not do. Section 280E does not rewrite the definition of gross income. Cannabis taxpayers generally still reduce gross receipts by COGS, because COGS is treated as an offset in arriving at gross income rather than a “deduction” in the §162 sense. Courts have repeatedly reflected this structure while disallowing operating expenses.

Case law that drives how audits are argued and won

The courts have largely reinforced two points:

Separate trades or businesses can matter, but only if real.

- In CHAMP, the Tax Court held a taxpayer had two trades or businesses (caregiving services and cannabis provision), allowing deductions allocable to the non-trafficking caregiving business while applying §280E to the cannabis activity.

- By contrast, in Olive, the Tax Court (affirmed by the Ninth Circuit) found the “primary” business was selling cannabis and that related services were not a separate trade or business where they were not separately charged and were inseparable from cannabis sales.

- The Harborside litigation is a modern anchor: the Tax Court applied §280E broadly and rejected attempts to treat branding/non-cannabis sales as separate where economics and operations were tightly integrated.

Inventory accounting is constrained: courts and IRS focus on the boundary between COGS and disallowed “deductions.”

The IRS and courts have repeatedly forced cannabis taxpayers back to §471 and the regulations, and have rejected “bootstrapping” nondeductible expenses into inventory via §263A in the cannabis context.

COGS, inventory, and capitalization: where most federal tax work actually happens

Resellers vs producers: the Tax Court and Ninth Circuit draw a bright line

For a purchaser-reseller, inventory cost is generally determined under Treas. Reg. §1.471-3(b) as the invoice price plus “transportation or other necessary charges incurred in acquiring possession” of the goods. The Ninth Circuit explicitly upheld applying this reseller rule to a dispensary and rejected arguments to include more expenditures in inventory as COGS.

For producers (cultivators and manufacturers), §1.471-3(c) and related inventory principles can allow a broader set of direct/indirect costs to be included in inventory compared with a pure reseller, but the boundary remains highly scrutinized under §280E audit posture.

IRS Chief Counsel Advice (CCA) and the “no §263A expansion” problem

A widely-cited IRS Chief Counsel Advice explains the IRS position that:

- §280E disallows deductions, but COGS remains allowable as an adjustment to gross receipts.

- Cannabis taxpayers may not use §263A to capitalize otherwise disallowed expenses into COGS; instead, they must use §471 methods as they existed when §280E was enacted.

That posture is consistent with later Tax Court analysis rejecting §263A capitalization for cannabis businesses.

Accounting methods and changes: §471 is the foundation; method changes can be high stakes

Most cannabis businesses still live inside the familiar choices of cash vs accrual, and inventory accounting methods under §471, but cannabis is unusual because the IRS often audits method boundaries and reclassifications that affect COGS (and therefore taxable income). The Tax Court’s Richmond Patients Group opinion is a practical example of how facts and substantiation drive outcomes.

Practical framing: in cannabis, “inventory method” is not an accounting preference—it can be the difference between paying tax on near-gross profit versus something closer to economic profit.

Depreciation, fixed assets, and basis in a §280E world

Depreciation is generally a deduction (IRC §167/§168), so for a trade or business subject to §280E, depreciation that would otherwise be a normal operating deduction may be disallowed unless it is properly included in inventoriable costs under the applicable inventory rules for a producer (where supportable). The dispute typically isn’t whether depreciation exists—it’s whether it can be included in inventory under the applicable inventory provisions without running into the “disallowed deduction” wall. The IRS and courts’ emphasis on §471 boundaries is why fixed-asset/inventory classification is a recurring audit issue.

Basis still matters. Even when deductions are denied, the tax law still relies heavily on basis for inventory, property dispositions, and certain capitalization rules. Cannabis businesses should treat basis schedules (inventory layers, fixed asset subledgers) as “audit-ready” files, not back-office artifacts.

Tax credits and R&D credits: “if applicable” usually means “only outside trafficking”

§280E disallows credits as well as deductions when they are tied to the trafficking trade or business. That makes common credit strategies—including potentially R&D credits under §41—fact-dependent and often limited to truly separate non-trafficking activities (if any). This is one reason sophisticated operators sometimes structure genuine non-trafficking R&D, IP development, equipment design, or data/analytics businesses separately, with strong transfer pricing and operational separation—because courts examine facts, not labels, when deciding whether activities are separate trades or businesses.

Payroll taxes, information reporting, and estimated taxes: §280E doesn’t change the rules

Employment taxes are still fully due. Cannabis employers must withhold, deposit, report, and pay employment taxes like any other employer. Publication 15 is the primary baseline reference.

Employment tax filing deadlines are standard. For example, quarterly Form 941 returns are generally due April 30, July 31, Oct. 31 and Jan. 31, with a 10-day extension in certain timely-deposit situations. See Employment tax due dates.

Estimated tax payments still apply. The IRS explicitly warns that underpaying by each payment period can trigger penalties even if you ultimately receive a refund when filing the annual return. Cannabis taxpayers are at higher risk because §280E commonly drives higher taxable income than the P&L suggests.

Timeline of major federal tax milestones that still shape 2025 practice

State tax regimes and comparative analysis

Scope and state list

This report covers 40 states with comprehensive medical cannabis programs as of June 26, 2025, and flags which of those also have adult-use legalization (24 states). The list is sourced from a consolidated state-by-state legal program tracker.

States covered: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Florida, Hawaii, Illinois, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Dakota, Texas, Utah, Vermont, Virginia, Washington, West Virginia.

How to read state cannabis taxes

Most states combine some mix of these layers:

- Cannabis-specific taxes (excise, gross receipts, weight-based, potency-based, or per-ounce fees).

- General sales taxes (where the state has one), often plus local sales taxes.

- Local cannabis taxes (local option excise, transfer taxes, gross receipts, etc.).

- Licensing and application fees (often tiered by canopy, revenue, or license class; frequently city/county-level too).

On state income taxes, the business question is less about the tax rate and more about whether the state:

- Conforms to federal taxable income and therefore inherits much of §280E’s denial, or

- Decouples for cannabis (partially or fully), allowing expenses disallowed federally to be deducted for state income tax.

Comparative table of adult-use states

This table focuses on adult-use taxes and the major “stacking” features that affect compliance design. “Deductibility vs federal” is shown as “decouples” where public summaries state that the state allows cannabis business deductions for state income tax despite §280E, otherwise “conforms/unclear,” and “N/A” where state income tax is not the main lever (e.g., no personal income tax).

| State | Adult-use status | State cannabis-specific tax (adult-use) | Sales tax on cannabis | Local cannabis taxes / special notes | State income tax deductibility vs federal §280E |

|---|---|---|---|---|---|

| Alaska | Legal/regulated | Cultivation excise tax: $50/oz (statute baseline; additional rates exist by product type) | No statewide sales tax | Local sales taxes may apply | N/A (state-level income tax treatment unspecified) |

| Arizona | Legal/regulated | 16% excise on retail sales | Transaction privilege tax (TPT) applies (rate varies) | Local TPT applies (varies) | Conforms/unclear (not listed as decoupling) |

| California | Legal/regulated | Cannabis excise: 15% (Jan 1, 2023–Jun 30, 2025); 19% (Jul 1–Sep 30, 2025); 15% (Oct 1, 2025–Jun 30, 2028) | State sales tax applies (base 7.25% plus local) | Local cannabis business taxes common (rates vary by city/county) | Decouples (confirm with CA law/returns) |

| Colorado | Legal/regulated | 15% excise on first sale/transfer at AMR or contract price | 15% retail marijuana sales tax on consumer purchase | Local sales taxes may apply (varies) | Decouples (confirm in CO law/returns) |

| Connecticut | Legal/regulated | Statewide cannabis tax based on THC mg (e.g., $0.00625/mg flower; $0.0275/mg edibles; $0.009/mg other) | 6.35% sales tax applies | 3% municipal tax, plus THC-based tax above | Decouples (confirm in CT law/returns) |

| Delaware | Legal/regulated | Retail marijuana tax: 15% of retail sales price | Unspecified in this report | Local option taxes: unspecified | Decouples (confirm in DE law/returns) |

| Illinois | Legal/regulated | Cultivation privilege tax: 7% of first sale; Purchaser excise: 10% / 20% / 25% depending on product/potency | Sales/use taxes apply; local rates vary | Local taxes may apply (varies) | Decouples (confirm in IL law/returns) |

| Maine | Legal/regulated | Retail tax 10%; plus weight-based excise (e.g., $335/lb flower; $94/lb trim; per plant/seed) | 5.5% sales tax applies (adult-use) | Local option: none listed in cited state summary | Decouples (confirm in ME law/returns) |

| Maryland | Legal/regulated | Adult-use cannabis taxed via sales & use tax: 9% originally; increased to 12% effective July 1, 2025 (tax-year split) | Included above (sales & use tax mechanism) | Local cannabis tax: unspecified | Decouples (per multi-state summaries; confirm in MD law/returns) |

| Massachusetts | Legal/regulated | 10.75% excise tax on adult-use sales | 6.25% sales tax applies | Local option up to 3% (host community) | Decouples (confirm in MA law/returns) |

| Michigan | Legal/regulated | 10% retail excise (MRE tax) | 6% sales tax applies | No local excise listed in cited state treasury summary | Decouples (confirm in MI law/returns) |

| Minnesota | Legal/regulated | Cannabis gross receipts tax: 15% (effective July 1, 2025; earlier rate lower) | 6.875% sales tax plus local sales taxes | Local sales taxes may apply (varies) | Decouples (confirm in MN law/returns) |

| Missouri | Legal/regulated | Adult-use: 6% tax on retail sale | General sales taxes also apply (rates vary by locality) | Local option up to 3% exists; MO Supreme Court limited stacking (city or county in incorporated areas) | Decouples (confirm in MO law/returns) |

| Montana | Legal/regulated | 20% state tax on adult-use; 4% medical; local option up to 3% | No statewide sales tax | Local-option county tax up to 3% | Decouples (confirm in MT law/returns) |

| Nevada | Legal/regulated | 10% retail excise (adult-use only; not for patient cardholders) | Sales tax applies (rates + local) | Also has wholesale cannabis excise | N/A (state income tax treatment unspecified) |

| New Jersey | Legal/regulated | SEEF: $2.50/ounce beginning Jan 1, 2025; imposed on cultivator sale/transfer (not retail consumers) | Recreational cannabis retail sales are subject to sales & use tax | Local cannabis transfer tax up to 2% | Decouples (confirm in NJ law/returns) |

| New Mexico | Legal/regulated | Cannabis excise: 12% prior to July 1, 2025; 13% starting July 1, 2025; scheduled annual increases to 18% by July 2030 | Gross receipts tax applies (location-based rates) | Local GRT varies by location | Decouples (confirm in NM law/returns) |

| New York | Legal/regulated | Adult-use cannabis tax rates effective for sales on/after June 1, 2024: 9% distributor tax; 13% retail taxes total | State retail taxes shown above are specific cannabis taxes; general sales tax treatment not specified | Must complete licensing/registration with OCM and Tax Dept. | Decouples (confirm in NY law/returns) |

| Ohio | Legal/regulated | 10% excise tax on adult-use purchases | Regular sales taxes also apply (unspecified) | Local cannabis excise not indicated | Conforms/unclear (not listed as decoupling) |

| Oregon | Legal/regulated | 17% state marijuana tax | Oregon has no general sales tax | Local up to 3% with voter approval | Decouples (confirm in OR law/returns) |

| Rhode Island | Legal/regulated | 10% state cannabis excise tax | 7% sales tax applies | 3% local cannabis excise tax | Decouples (confirm in RI law/returns) |

| Vermont | Legal/regulated | 14% excise tax (retail price) | State sales tax applies (rate unspecified) | Local tax: unspecified | Decouples (confirm in VT law/returns) |

| Virginia | Adult-use legalization enacted; retail market status varies | Adult-use framework referenced with 21% retail tax + possible 3% local option (implementation timing can change) | Sales tax treatment: unspecified | Local option noted above; retail operations timing is a critical compliance variable | Conforms/unclear (not listed as decoupling) |

| Washington | Legal/regulated | 37% cannabis excise tax on retail selling price | General state/local sales taxes also apply (rate varies) | Medical exemption exists in statute (details depend on product/authorization) | N/A (income tax not the primary lever; B&O/sales/excise dominate) |

Licensing fees: Many adult-use states impose significant application and renewal fees by license class and size. This guide does not provide a complete fee schedule per state because fees commonly vary by license type (cultivator/manufacturer/retailer/distributor), capacity, and local jurisdiction; where not stated, the detail is “unspecified”. (State program links and license references exist in the legal program tracker.

Medical-only states: baseline tax notes and §280E decoupling signals

Where the state income tax treatment is publicly summarized as allowing deductions despite §280E, it is shown; otherwise “conforms/unclear.”

| State | Market status | State income tax deductibility vs federal §280E |

|---|---|---|

| Alabama | Medical only | Conforms/unclear |

| Arkansas | Medical only | Decouples |

| Florida | Medical only | Conforms/unclear |

| Hawaii | Medical only | Decouples |

| Kentucky | Medical only | Conforms/unclear |

| Louisiana | Medical only | Decouples |

| Mississippi | Medical only | Conforms/unclear |

| Nebraska | Medical legalized (industry regulation enacted; implementation status varies) | Conforms/unclear |

| New Hampshire | Medical only | Conforms/unclear |

| North Dakota | Medical only | Conforms/unclear |

| Oklahoma | Medical only | Conforms/unclear |

| Pennsylvania | Medical only | Decouples/partial (varies) |

| South Dakota | Medical only | Conforms/unclear |

| Texas | Medical only (program scope evolved in 2025 per legal tracker) | Conforms/unclear |

| Utah | Medical only | Conforms/unclear |

| West Virginia | Medical only | Conforms/unclear |

Note: State excise/sales/local/license fee details frequently change and should be pulled from each state’s revenue department and cannabis regulator for operational compliance.

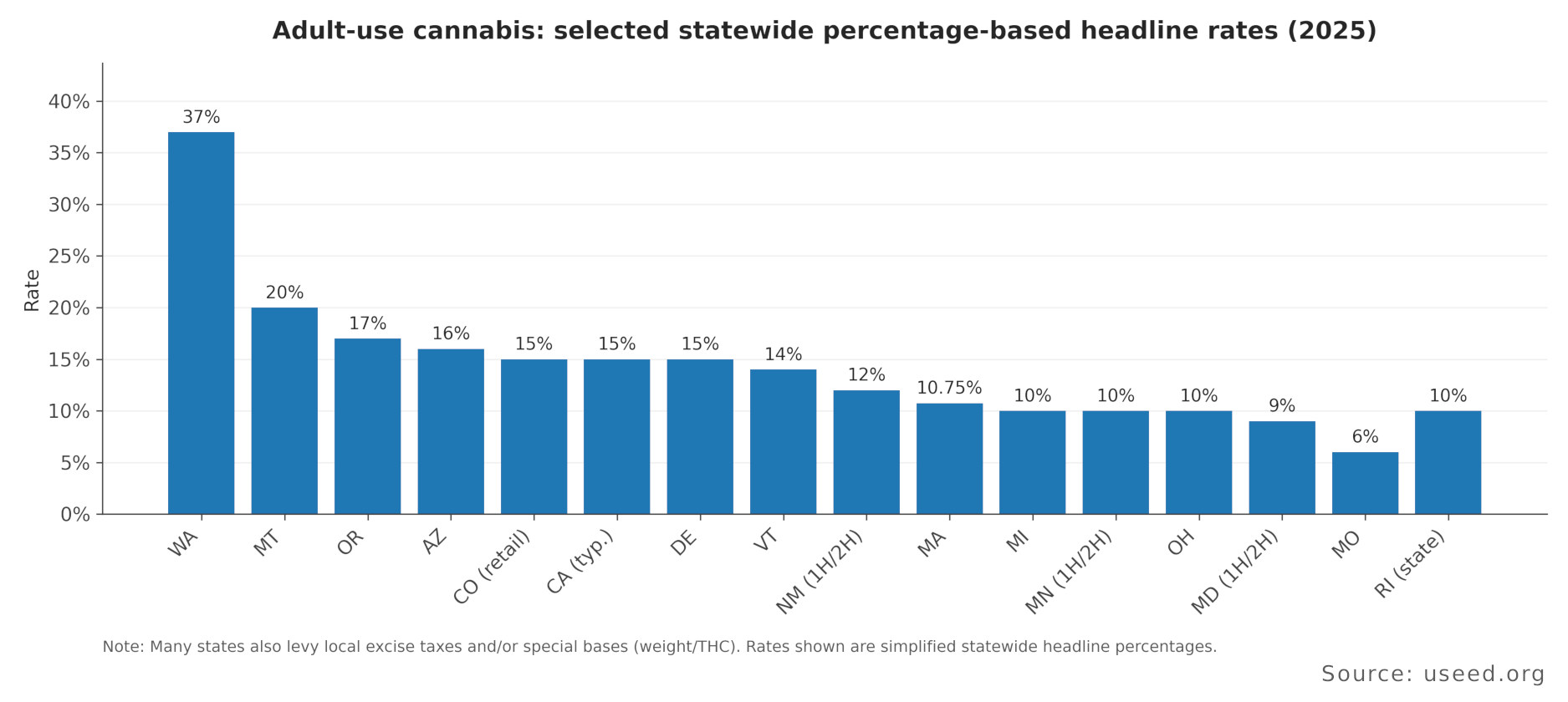

Bar chart: headline adult-use “state-level” rates (only where comparable)

The chart below compares a simplified “headline statewide rate” for adult-use cannabis where the tax is broadly percentage-based at retail (or the closest commonly cited state-level percentage). It excludes weight-based, potency-based, and per-ounce fee regimes because those are not comparable to ad valorem retail rates.

Sources (by state): Washington 37%; Montana 20%; Oregon 17%; Arizona 16%; Colorado 15%; California 15% typical with 2025 mid-year swing; Massachusetts 10.75%; Michigan 10%; Ohio 10%; Missouri 6%; Delaware 15%; Rhode Island 10% state excise; Vermont 14%; New Mexico 12% to 13% mid-2025; Minnesota 10% to 15% mid-2025; Maryland 9% to 12% mid-2025.

Compliance and planning best practices

Recordkeeping that survives a §280E + inventory audit

Design your books around audit questions, not management questions. The recurring litigation theme is that courts decide based on facts, documentation, and credible cost classification—especially when taxpayers attempt to increase COGS. The Richmond Patients Group opinion is a good reminder that inventory/COGS positions can fail when documentation is weak or the taxpayer’s characterization doesn’t match operational reality.

Minimum “audit-ready” files:

- Sales support: POS reports, seed-to-sale reports, invoices, bank deposits/cash logs, void/refund logs.

- Inventory support: beginning/ending counts, shrink logs, destruction logs, transfer manifests, bill of materials (manufacturing), and production batch records.

- Cost accounting workpapers: clear classification between inventoriable costs and non-inventoriable costs, with tie-outs to GL and payroll registers.

- Legal/operational structure support: org charts, management agreements, intercompany allocations, and evidence that purported non-trafficking activities have separate revenue streams (when asserted).

Inventory methods and cost strategies by business type

Retailers (pure resellers):

Expect the IRS to apply the reseller inventory rule (invoice price + acquisition costs) and to resist attempts to push general operating expenses into inventory. The Ninth Circuit’s Harborside decision specifically endorsed this approach for a dispensary treated as a reseller.

Cultivators and manufacturers (producers):

You generally have more plausible inventory capitalization opportunities than retailers because production inherently includes direct and some indirect costs. The practical constraint is that §280E and the IRS’s CCA posture restrict “extra” capitalization that looks like converting disallowed deductions into COGS.

Distributors:

Your treatment often depends on whether distribution is separate from retailing/manufacturing and whether you are a reseller vs producer. Where distributors are structurally and economically integrated with retail operations, courts tend to see one trafficking business unless facts demonstrate otherwise.

Entity selection and structuring: keep it simple unless you can prove separation

A common planning goal is to isolate non-trafficking activities (e.g., management services, consulting, IP development, non-cannabis retail) from the cannabis trafficking business. The case law shows why: CHAMP succeeded because the non-trafficking business was real and substantial, whereas Olive/Harborside emphasize that “incidental” activities don’t create a separate trade or business just because you want separate deductions.

Practical rule: If revenue, staff, facilities, and customer transactions are not separable in reality, separation on paper often collapses under examination.

Payroll compliance: don’t let §280E distract you from trust taxes

Employment tax compliance is not optional, and cannabis businesses should assume heightened scrutiny because payroll is one of the easiest enforcement levers. Publication 15 is the baseline framework for withholding, depositing, reporting, and paying employment taxes.

Sales/excise collection: build “multi-layer tax engines,” not flat-rate assumptions

Because states often layer (i) cannabis excise, (ii) sales tax, and (iii) local cannabis taxes, your POS and tax reporting should be set up to:

- capture the correct tax base (price vs THC mg vs weight),

- apply jurisdictional logic (local additions, special rules for medical cardholders), and

- map each tax stream to the right return and filing cadence.

Examples of “non-flat” structures: Connecticut THC mg tax + municipal tax; Illinois potency-tiered purchaser excise plus cultivation tax; Nevada retail vs medical differential on the 10% excise.

Cash-heavy operations and banking: compliance obligations that frequently get missed

Cash reporting (Form 8300):

If you receive more than $10,000 in cash in a trade or business (including related transactions), you generally must file Form 8300 within 15 days of the triggering payment. This is a common compliance failure in cash-heavy industries.

Banking and BSA reality (FinCEN):

FinCEN’s guidance explains how financial institutions may provide services to marijuana-related businesses consistent with Bank Secrecy Act expectations, including the use of SAR reporting categories. Practically, it does not make banking “easy,” but it is a foundational document shaping why banks require intensive KYC/monitoring from cannabis clients.

DOJ parallel guidance:

DOJ issued contemporaneous guidance regarding marijuana-related financial crimes, reinforcing why banks and vendors are conservative with cannabis exposures.

Filing, audit risk, penalties, and dispute resolution

Core federal forms and filing cadence

Income tax returns depend on entity type:

Employment tax filings:

Quarterly employment tax filing due dates are summarized by the IRS (for example, Form 941 due the last day of the month following each quarter).

Estimated tax:

The IRS explains the four-period structure and penalty exposure if you underpay by each period.

Common audit triggers in cannabis (fact patterns courts repeatedly evaluate)

While the IRS does not publish a public “cannabis audit checklist,” the litigation record shows recurring pressure points:

- Aggressive COGS/inventory inclusion (especially for retailers attempting producer-like capitalization). The Harborside and Richmond Patients Group decisions show the IRS and courts’ focus on inventory rules and substantiation.

- Claimed “separate business” deductions without separate revenue, staffing, or operational substance (Olive; Harborside).

- Cash-handling compliance failures, including Form 8300 rules, which are explicitly emphasized by the IRS for trades or businesses receiving >$10,000 in cash.

Disputes and resolution pathways

Federal disputes generally follow the standard escalation ladder: exam → proposed adjustments → administrative appeals → litigation (Tax Court or refund suit posture). Cannabis cases frequently turn on documentation and aligning operations with the taxpayer’s asserted trade/business and inventory method. The volume of cannabis §280E litigation and repeated defeats on “relabeling” theories is why many taxpayers focus on defensible COGS, clean recordkeeping, and conservative positions with protective documentation rather than novel theories.

Open issues and outlook through 2026

Scheduling reform and the §280E “off switch”

Because §280E is explicitly tied to Schedule I and II controlled substances, moving marijuana out of Schedule I/II would directly change the federal tax posture for many cannabis operators. §280E’s text makes this linkage explicit.

Continued litigation pressure on “what is COGS” and “what is a separate business”

As of 2026 practice, the most durable lessons remain:

- Courts apply §280E broadly when trafficking is present.

- Attempts to expand inventory capitalization beyond what the regulations support face resistance, especially for reseller models.

- “Separate business” arguments can work, but only with real separation and real economics.

State-level developments that materially reshaped 2025 compliance workloads

- California adjusted its excise rate twice during 2025 (mid-year increase then rollback), increasing the importance of correct POS configuration, invoice language, and month-by-month tax mapping.

- Minnesota increased its cannabis tax rate effective July 1, 2025, stacking on top of sales tax and local sales taxes—again raising the importance of correct jurisdiction and rate application.

- New Mexico moved into its scheduled annual increases starting July 1, 2025, with explicit state guidance describing the step-up schedule.

These changes underline a practical truth: in cannabis, tax compliance is operational, not just annual, as rate changes often take effect mid-year, and the cost of being wrong is usually not just tax, but penalties, license risk, and costly remediation.