Introduction

Federal cannabis rescheduling is underway but still pending. A Dec 2025 White House order instructed the Attorney General to finalize rescheduling marijuana from Schedule I to III of the CSA. As of early 2026, final action is not yet taken, and legal challenges remain.

The biggest financial effect of Schedule III will be the end of Section 280E of the tax code. Today, 280E forces cannabis businesses (as Schedule I/II “traffickers”) to pay tax on gross revenue with almost no deductions. Removing 280E means companies can deduct normal costs (payroll, rent, marketing, etc.) just like any other business. In practice, this dramatically boosts profits and cash flow.

For example, Curaleaf has estimated about $150 million in annual federal tax savings under a Schedule III status. Similarly, analytics firm Headset finds a typical dispensary loses roughly $268,000 per year in federal taxes due to 280E. Industry-wide, Headset estimates $1.6–$2.2 billion per year of after-tax cash flow would be freed up once 280E is gone.

Besides taxes, rescheduling may also bring modest revenue gains (new medical products, research access) and lower costs (less extreme compliance, partial banking access). We quantify these effects in conservative vs. optimistic scenarios below. Even a Schedule III outcome (no 280E) can more than double after-tax margins. Full descheduling (federal legalization) unlocks still larger upside.

We also cover impacts on financing and valuation (lower cost of capital, higher multiples) and accounting (amortizing licenses, R&D expensing). The guidance sections at the end explain modeling adjustments, disclosure tips, and risk factors to monitor.

Federal Rescheduling Status and Timeline

Current law: Marijuana is Schedule I (no accepted medical use, high abuse) under the Controlled Substances Act (CSA). DEA (within DOJ) has scheduling authority but must seek HHS/FDA scientific review first. In late 2022, President Biden asked for just that. By Aug 2023 HHS had agreed cannabis meets medical-use criteria and recommended Schedule III.

In May 2024 the DOJ/DEA put out a proposed rule to move cannabis from I to III. This triggers a public comment period and, if requested, a hearing. Over 42,000 comments were submitted, and a hearing was scheduled for Jan 2025, but an internal appeal delayed that process.

On Dec. 18, 2025, President Trump issued an executive order directing DOJ to expedite finalization of the rule rescheduling cannabis to Schedule III. The EO also orders agencies to improve CBD product access. The EO does not itself remove cannabis from the CSA; it just tells DEA/DOJ to finish the rulemaking “in the most expeditious manner”. DEA has said only that the process “remains pending.”

Timeline: The timeline above highlights key steps. After final rulemaking, there can still be court challenges (some parties already asked the courts to order DEA to act). The exact schedule remains uncertain. Stakeholders should assume any rule (if issued) would have a future effective date (likely months after publication). For tax and financial planning, the IRS may wait until the next calendar year to apply the new rule, so benefits might not appear until the following tax year.

Key Agencies

- DEA/DOJ: DEA (under the Attorney General) makes the scheduling decision by rule. DOJ’s Office of Legal Counsel and Attorney General provide legal views (e.g. OLC approved HHS’s medical-use test in Apr 2024). The Administrative Law Judge at DEA can hold hearings on the rule.

- HHS/FDA: HHS (via FDA and NIH) does the medical/scientific review and gives a recommendation to DEA, which is binding at the proposal stage. FDA will still regulate cannabis drugs under its rules (no auto-FDA approval from rescheduling, but scientific research is easier).

- IRS/Treasury: The IRS enforces §280E and other tax laws. Treasury (FinCEN) regulates banks (the SAFE Banking Act has never passed the senate). Rescheduling may prompt new guidance from IRS/Treasury on tax treatment and banking.

- Other agencies: FDA (see above), and possibly ONDCP or DEA Diversion Control for enforcement. Treasury’s fintech agencies (e.g. OCC, Fed) will decide on bank access if cannabis becomes legal.

Tax and Profit Implications

Section 280E today: Since cannabis is Schedule I, IRC §280E forces companies to pay tax on gross income (revenue) with no deductions except Cost of Goods Sold. In practice, this means operating at very high effective tax rates. Congressional researchers note many operators face federal tax rates as high as 70–80%. In fact, current tax rules help explain why only ~27% of U.S. cannabis businesses were profitable in 2024, versus ~65% in normal small businesses.

Schedule III effect: Rescheduling to Schedule III would eliminate 280E’s restrictions. EisnerAmper observes that once reclassified, 280E “may no longer restrict cannabis companies from taking deductions or credits”. In practical terms, companies could deduct all ordinary expenses (payroll, rent, marketing, utilities, etc.) instead of only COGS. AAFCPAs notes this “dramatically improves cash flow and profitability”. Effective federal tax rates would collapse from ~70% down to the normal 21% (plus modest state tax, say ~4–9%), i.e. ~25–30% combined. (Some states may still conform to the higher tax base; many already decoupled 280E.)

Quantifying the change: The profit boost is enormous. For example, Curaleaf forecasts about $150 million in federal tax relief in 2024 alone if Schedule III were in place. Headset’s median-store model finds a Schedule I retailer loses ~$268k/year to 280E (federal tax). Industry-wide, Headset estimates $1.6–$2.2 billion of extra after-tax cash flow at current sales levels once 280E is gone. In other words, money that now goes straight to Uncle Sam becomes available to cannabis businesses to reinvest or return to shareholders.

Other tax provisions: The timing of tax-year changes matters. If the final rule comes into effect partway through a year, companies will only get deductions on expenses incurred after that date. For example, if a rule is finalized in early 2026, IRS has suggested calendar-year filers might not see benefits until 2027. Also, the corporate tax landscape is slightly sweeter now: 2022’s “One Big Beautiful Bill” revived 100% bonus depreciation and expanded §179 expensing. EisnerAmper notes cannabis firms would fully leverage those provisions on post-reschedule equipment purchases. In short, a rescheduled industry not only sheds 280E but can also use modern tax benefits on new investments, further boosting cash flow.

Profit Scenarios (After-Tax Impact)

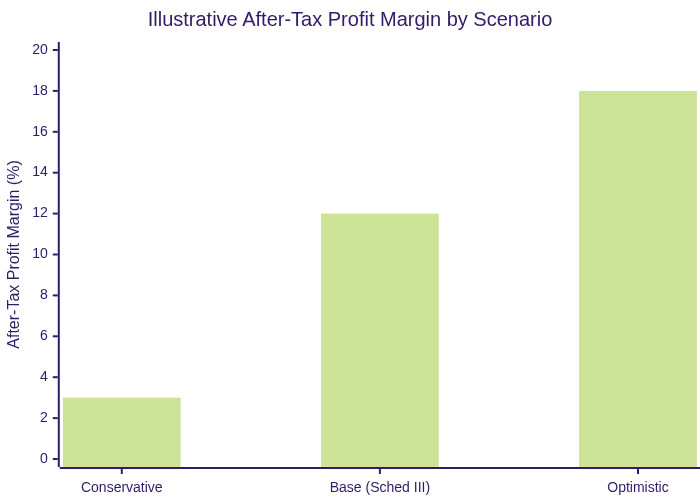

We can illustrate with three scenarios for a hypothetical operator:

| Scenario | Federal Status | Rev. Growth | Effective Tax | After-Tax Profit Margin (est.) |

|---|---|---|---|---|

| Conservative | Remains Schedule I | +~5% (flat) | ~70% | ~0–5% (thin/negative) |

| Base (Sched III) | Schedule III | +~10% | 25–30% | 10–15% |

| Optimistic | Descheduled/legal | +~20% | 25–30% | 15–20% |

Conservative (Status Quo): 280E stays fully in place, so the operator pays ~70% tax on its pre-tax profit. Even if the company makes 10% EBITDA, most of that vanishes in taxes, leaving near-zero or negative net profit. Cannabis margins stay very tight or negative.

Base Case (Schedule III): 280E is removed. The company’s effective tax rate drops to ~25–30%. This means the same 10% EBITDA now yields ~7–8% net profit margin after tax (we estimate). In practice, operators would likely reinvest a portion, but the margin roughly doubles. A few lines of deductible expenses (wages, rent) yield an immediate ~8-12 percentage point net margin swing.

Optimistic (Full Legalization): Federal legality plus Schedule III. After-tax rate still ~25–30%. But with full commerce, we assume higher revenue growth (20%+) and continued cost efficiencies. Profit margins might reach ~15–20% of revenue. (This is speculative: actual margins depend on market pricing and competition, but it shows the ceiling when taxes and regulations normalize.)

Figure: Hypothetical after-tax profit margin under different federal outcomes. Conservative case yields near-zero profit; Schedule III (no 280E) yields double-digit profit; full legalization yields higher profit margin.

In other words, moving to Schedule III eliminates the tax penalty and effectively creates profit out of what is now pure tax expense. Many small-state operators could turn from losses to sizeable profits overnight.

Banking, Finance, M&A and Valuation

Rescheduling (especially legalization) substantially improves financial conditions. Banks will likely become more willing to lend and provide services. Even without new legislation, lowering cannabis to Schedule III reduces federal risk and encourages banks to reconsider partnerships. This means access to checking accounts, credit cards, loans and lower interest rates. Capital that was once trapped (in cash or high-interest debt) becomes available at normal terms.

Lower risk and higher cash flows justify higher valuation multiples. Cannabis public stocks currently trade at depressed multiples: median EV/Revenue is only ~1× as of late 2023 (versus 5–13× in 2020–21). With strong EBITDA and normal tax rates, companies could command multiples in line with other health/consumer industries.

For example, Withum notes that eliminating 280E “can support higher valuation multiples as companies demonstrate scalable operations and improved profitability”. M&A activity should pick up: buyers would value firms on actual cash earnings instead of penalizing them for tax inefficiencies. Public cannabis stocks did react positively to the Dec 2025 reschedule news, though pricing in depends on timeline risk.

Accounting (GAAP) also changes. Today, many U.S. cannabis companies use IFRS or carve-outs because GAAP has no special rule for illegal businesses (see our cannabis accounting and cannabis bookkeeping guides). Intangible assets like cultivation licenses are often not capitalized (or immediately impaired) under GAAP. If cannabis is legalized federally, firms could start recognizing and amortizing licenses, patents, and other intangibles. Also, business combinations might be treated more like normal M&A (with goodwill, etc.) instead of inherently “illegal” assets. This would reduce volatility in earnings when deals occur.

Guidance for Operators and Investors

Modeling adjustments: Analysts should build in reduced tax rates and restored deductions for O&M, security, marketing, etc. Add scenario lines for increased revenue from expanded markets. For example, include a case where the effective tax rate falls to ~25% and OPEX drops by 20–50%. Also model the timing: if final rule comes in 2026, allow lost deductions in that year and full benefit afterward.

Disclosure: Companies should disclose the uncertainty around federal status in MD&As and risk factors. Material estimates should note that EBITDA, net income, and cash flow could change dramatically if rescheduling occurs. SEC filings of many MSOs already discuss 280E risks; they may now also discuss potential schedule change as both risk and opportunity. Earnings calls should clarify how tax-loss NOLs might be used if 280E ends.

Tax planning: Work with tax advisors to file amended returns or elections as appropriate once rescheduling is certain. Because final IRS guidance may lag, some companies may file protective claims or revise tax accounting (e.g. reclassify deferred tax assets). Management should also assess timing: for example, delaying some expenses into the first full tax year under Schedule III, or accelerating capex to maximize bonus depreciation.

Risk factors: The biggest near-term risk is timing: if DEA finalizes in late 2026 or later, benefits are delayed. There is also legislative risk (Congress could amend law) or legal risk (courts could vacate DEA’s rule). Interest rates and inflation also affect financing cost independent of policy. Finally, even descheduling would not eliminate state taxes or state regulatory compliance; state frameworks remain in flux.

All things considered, federal rescheduling is fundamentally a tax event. A move to Schedule III (and eventual descheduling) doesn’t change plants or prescriptions overnight, but it multiplies profits and cash flow. Cannabis executives and investors should focus their models on post-280E tax rates and NOL usage, not just EBITDA. When 280E goes away, an industry that is largely unprofitable today could become much more profitable… and every dollar saved from Uncle Sam falls straight to the bottom line.