Introduction

U.S. cannabis accounting is hard for one main reason: federal taxes treat state-legal cannabis as Schedule I trafficking, so IRC §280E blocks ordinary deductions and credits, leaving COGS as the primary path to reduce federal taxable income.

That single constraint drives most of the industry-specific accounting practices:

Federal tax rules

IRC §280E denies deductions/credits for amounts paid or incurred in a trafficking trade or business.

COGS remains allowed, but the amount you can treat as COGS depends on whether you are a reseller (retail/distribution) or a producer (cultivation/manufacturing) under the inventory rules. For cannabis businesses, the IRS has taken the position that §263A cannot be used to capitalize otherwise disallowed §280E costs (the “flush language” problem). COGS generally must be computed under §471 rules (and the applicable regulations).

State rules

States often decouple from §280E for state income taxes (or don’t levy income tax at all). This creates a practical reality: you still book GAAP expenses fully, but you may have very different taxable-income calculations by jurisdiction.

GAAP reporting

For financial reporting under U.S. GAAP, cannabis companies follow the same core standards as any consumer/CPG operator: ASC 606 for revenue, inventory at cost with modern lower-of-cost/NRV rules, and robust disclosures around estimates and risks.

Operational playbook

The practical winning move is disciplined cost accounting + inventory controls + cash controls: batch/lot-level costing tied to seed-to-sale, POS-to-bank/cash reconciliation, defensible shrink/waste tracking, and audit-ready documentation that supports your COGS position and excise/sales tax filings.

Scope and key assumptions

This guide covers state-licensed cannabis operators (adult-use and/or medical) that touch the plant: cultivation, manufacturing, distribution/wholesale, and retail. Federal illegality constraints and banking friction are treated as operating realities.

Assumptions

- Financial reporting framework: U.S. GAAP (accrual basis). Core GAAP references: ASC 606 (revenue) and modern inventory measurement guidance.

- Tax posture: Cannabis remains a Schedule I drug at the federal level in the current rule set described by the DEA, so §280E is still “live” for federal income tax planning unless/until rescheduling is finalized through rulemaking.

- Business complexity: Could be single-entity or multi-entity; could be single-state or multi-state.

Not legal/tax advice

As cannabis laws frequently change, you should always refer to current local and federal laws to ensure compliance.

Federal tax rules and the COGS-centered reality

IRC §280E in one paragraph

IRC §280E says no deduction or credit is allowed for amounts paid or incurred in carrying on a trade or business that consists of trafficking in Schedule I or II controlled substances prohibited by federal law or the law of the state where conducted.

Because marijuana remains treated as Schedule I in federal controlled-substance scheduling (as described by the Drug Enforcement Administration), plant-touching cannabis operators generally get hit by 280E at the federal level even if fully licensed by their state.

What’s left after 280E

- You still recognize gross income normally.

- You still keep GAAP books normally.

- For federal tax, COGS is the principal mechanism to reduce taxable income because COGS is part of computing gross income, not a “below-the-line” ordinary deduction. The operational consequence is that your accounting must support defensible inventory costing.

COGS rules: reseller vs producer

Most practical COGS disputes boil down to: “What can be inventoried?”

Resellers (typical retail dispensary; wholesale/distribution that buys finished goods)

Under inventory costing rules for purchased merchandise, “cost” generally starts with invoice price net of discounts and adds transportation or other necessary charges to acquire possession.

Key point: this is not a license to push store rent, retail payroll, marketing, or security into COGS. Those are classic operating expenses, and 280E denies them for federal tax purposes.

Producers (cultivation/manufacturing)

Manufacturers must use “full absorption” type principles for tax inventory costing: direct materials, direct labor, and a proper share of indirect production costs incident to production.

Practically, producers often have more legal room than retailers to include certain production-related indirect costs in inventoriable cost pools (e.g., grow labor, certain facility costs tied to production areas), but this must remain consistent with the inventory regulations—especially in an audit.

Why §263A usually doesn’t save you under 280E

Some industries capitalize costs under §263A (UNICAP) to shift more spend into inventory. Cannabis might seem like a candidate—until you hit the statutory “flush language” issue.

The Internal Revenue Service Chief Counsel memo (CCA 201504011) explains the IRS view: §263A is a timing rule and does not convert nondeductible costs into inventoriable costs, and §280E plus §263A(a)(2) flush language prevents getting a benefit by capitalizing costs that otherwise could not be taken into account.

Bottom line for planning: assume the IRS will challenge “COGS inflation” strategies that look like disguised OPEX capitalization.

Accounting method, inventories, and the small business rules

Inventory often forces accrual accounting for purchases and sales when inventory is an income-producing factor, subject to certain small business exceptions and method choices.

When cannabis operators try to use small-business inventory rules to increase COGS, the risk is not theoretical: the IRS has trained on cannabis reporting and explicitly flags §§280E and 471 and method-of-accounting issues.

Practical federal-tax deliverables you should maintain:

- Written inventory capitalization policy (reseller vs producer logic; cost pools; allocation drivers).

- Batch/lot costing workpapers tied to supporting docs (timekeeping, BOMs, invoices).

- A tax workpaper that separates: (1) COGS, (2) deductible expenses (if any non-plant-touching lines exist), (3) 280E-disallowed expenses.

Payroll, credits, and employment taxes under 280E

280E frequently surprises operators in two ways:

First, it’s not a payroll-tax exemption.

You must still run compliant payroll, withhold and remit employment taxes, and file/pay on required deposit schedules.

Second, federal credits are not your friend under 280E.

Because the statute denies credit tied to a trafficking trade or business, general business credits and certain incentive credits may be unavailable (or severely constrained) for plant-touching entities.

That does not mean you ignore credits; it means you evaluate eligibility carefully by entity and activity.

Cash-intensive operations: Form 8300 and recordkeeping are not optional

Cannabis cash handling increases exposure to federal cash-reporting rules. If you receive more than $10,000 in cash in a trade or business, you generally must file Form 8300 within 15 days, and you must provide a written statement to the payer by January 31 following the year of the reportable transaction.

Also expect the IRS to care about your books: recordkeeping must be sufficient to substantiate income, deductions, and credits.

State tax variations in major markets

State tax outcomes vary across three dimensions:

- Income/franchise tax conformity to §280E (or the absence of income tax)

- Cannabis excise tax structure (retail-only vs multi-stage; potency-based; wholesale value bases)

- Sales tax interaction (whether sales tax applies in addition to excise, and what the “tax base” includes)

The table below is a practical snapshot (not a substitute for current-year state guidance). “Decoupled” means the state allows some or all ordinary deductions disallowed federally by §280E for qualifying licensed activity.

| Major market | State income tax doesn’t apply / §280E decoupling | Core cannabis excise / special taxes |

|---|---|---|

| California | Licensed cannabis businesses can deduct COGS and ordinary/necessary business expenses for CA purposes (licensed vs unlicensed is a key distinction). | State cannabis excise tax rate has changed over time; CDTFA rate table shows 15% effective Oct 1, 2025 (and other effective-date windows). |

| Colorado | Colorado provides a “Marijuana Business Deduction” for state income tax: expenditures eligible federally but disallowed by §280E. | Retail marijuana excise tax is 15% on Average Market Rate/contract price and retail marijuana sales tax is 15% (plus applicable local taxes). |

| Washington | No state income tax; WA uses a gross receipts B&O tax with no deductions for costs. | WA is a high-excise state with retail-level excise commonly cited at 37% (verify current WA cannabis tax rules). |

| Oregon | OR law limits §280E’s application in Oregon corporate taxation for conduct authorized under Oregon cannabis statutes (state-level relief for authorized activity). | OLCC retailers charge 17% state retail tax; some localities add up to 3% local tax, administered in many cases via Oregon DOR. |

| Illinois | Illinois allows a modification for cannabis establishments: a subtraction for deductions disallowed under §280E (effective for tax years beginning on/after Jan 1, 2023 for licensed establishments). | Adult-use purchaser excise is tiered by THC/product type: 10% (≤35% THC flower), 25% (>35% flower), 20% infused products (plus general sales tax and other layers). |

| Massachusetts | MA enacted state-level relief decoupling from §280E for licensed marijuana businesses effective for tax years beginning on/after Jan 1, 2022. | 10.75% state excise plus up to 3% local option, and sales tax applies to adult-use retail (medical treated differently). |

| Michigan | Michigan Treasury guidance provides state-level relief from §280E for certain licensed marijuana businesses for MI purposes. | Adult-use: 10% excise plus 6% sales tax; Michigan also issued guidance for a new 24% wholesale-level excise tax beginning Jan 1, 2026 under CRFTA. |

| Arizona | Arizona law permits certain licensed marijuana taxpayers to subtract ordinary and necessary expenses disallowed federally under §280E when computing AZ income. | Adult-use: AZ DOR describes a 16% excise tax plus transaction privilege tax (TPT). |

| Nevada | No corporate income tax is a key feature cited by NV state sources; NV instead has gross-revenue type taxes like the Commerce Tax above thresholds. | NV cannabis excise includes a 15% wholesale excise (adult-use and medical) and a 10% retail excise (adult-use); state reporting references NRS 372A.290. |

| New York | NY provides a state subtraction/deduction for commercial cannabis activity expenses that are disallowed federally under §280E, effective for tax years beginning on/after Jan 1, 2022. | NY adult-use tax (via NY DTF): 13% retail taxes and distributor tax rules effective for sales on/after June 1, 2024; potency tax rates appear in historical DTF rate detail. |

State takeaway you should operationalize

Even when a state “decouples,” you often must track the §280E-disallowed expense amount for state reporting or modifications. That means your chart of accounts and class/location structure should preserve a clean “280E bucket” in the general ledger even though it’s still a GAAP expense.

GAAP and financial reporting issues that matter most in cannabis

This section is relevant for U.S. GAAP reporters (private companies, lenders, investors, or potential SEC registrants).

Revenue recognition: where cannabis has recurring traps

Under ASC 606, revenue is recognized to depict the transfer of promised goods/services in the amount of consideration expected. The standard uses a “step model” (identify contract → performance obligations → transaction price → allocate → recognize).

Cannabis-specific pressure points within that general model:

- Returns, price adjustments, and discounting: cannabis retail pricing can be dynamic (happy hours, loyalty tiers, managers’ comps). Your controls must ensure the POS discount logic maps correctly to revenue netting and promotional expense classification. The accounting question is less “can you discount?” and more “did you measure consideration correctly and consistently?”

- Excise and sales taxes: your financial statements must present revenue in a way consistent with whether you’re collecting taxes on behalf of a government (often net presentation). Cannabis operators should define, document, and apply a consistent policy for which taxes are “pass-through” vs part of transaction price. (ASC 606 is the anchor standard for this policy framework.)

Inventory valuation and cost absorption

U.S. GAAP inventory is measured at cost, with subsequent measurement guidance that (for many entities) uses lower of cost and net realizable value (NRV) rather than the older “lower of cost or market” model in many cases.

Cannabis inventory valuation tends to be unusually judgment-heavy because:

- Shelf life, batch failures, and regulatory destruction events can drive frequent write-downs.

- Shrink/waste must be measured and explained (and often ties directly into tax COGS support).

- Growth-cycle work-in-process (plants-in-progress) creates a need for clear stage-based cost accumulation.

The operational link to federal tax is direct: tax inventory costing rules define what can be capitalized into inventory/COGS (reseller vs producer distinctions), and cannabis cannot rely on §263A to “convert” disallowed costs into inventoriable costs per IRS Chief Counsel’s analysis.

Impairment, fair value, and licenses

Even without cannabis-specific GAAP, cannabis operators often face these patterns:

- Long-lived assets (buildouts, grow equipment) are sensitive to price compression and regulatory shocks, increasing impairment testing pressure.

- Licenses and license-related intangible value can be material in acquisitions; how you account depends on whether the license is acquired (business combination) vs internally developed. (Fair value and impairment topics frequently emerge through deal accounting rather than day-to-day operations.)

A fast, practical disclosure mindset:

ASC 606 explicitly expects disclosures that help users understand revenue’s nature, timing, uncertainty, and key judgments. Cannabis businesses should treat these disclosures as a checklist for: (a) pricing variability, (b) returns/allowances, (c) contract types (medical vs adult-use; wholesale vs retail).

Operational accounting playbook

Bookkeeping architecture and cost-center design

If your books can’t answer “what costs are inventoriable vs not,” you will struggle with both audits and tax planning.

Design principles:

- Use cost centers aligned to operational reality: cultivation rooms, extraction lab, kitchen/edibles line, packaging, distribution, retail store(s).

- Separate direct labor timekeeping by function (production vs retail vs admin). This is a core input to full absorption costing for producers and a core defense for what belongs in inventory.

- Maintain a clear “280E tracking layer” in reporting: you still book expenses, but you need a clean roll-forward for tax workpapers.

Recommended chart of accounts by business type

This table is a starting template. You should still tailor it to your license types and state reporting needs.

| COA area | Cultivation (producer) | Manufacturing (producer) | Retail (reseller) | Distribution/Wholesale (reseller or hybrid) |

|---|---|---|---|---|

| Revenue | Wholesale flower; wholesale biomass; internal transfers (eliminate in consolidation) | Wholesale finished goods; tolling; white-label fees | Retail cannabis sales; non-cannabis merchandise; delivery fees | Wholesale sales; transport fees (if separately priced) |

| Inventory accounts | Plants-in-progress (WIP); harvested WIP; finished flower; trim/biomass; supplies | Raw materials; packaging; WIP (by product line); finished goods | Finished goods inventory (by category); accessories inventory | Finished goods inventory; in-transit inventory; samples (controlled) |

| COGS accounts | COGS: cultivation (absorption); testing (if inventoriable under policy); production utilities (if allocable) | COGS: manufacturing; direct labor; packaging consumed; lab supplies | COGS: purchased goods; vendor freight-in | COGS: purchased goods; freight-in; repack labor (if allowed under policy) |

| Key operating expenses | Compliance/security; facility overhead not capitalized; admin payroll | QA/regulatory; R&D (book); depreciation; compliance | Store payroll; rent; marketing; POS fees; security | Sales payroll; warehousing; logistics; compliance |

| Taxes & fees | Cultivation taxes (state/local if applicable); license fees | Excise impacts (state-dependent); license fees | Sales tax payable; excise tax payable; local taxes | Excise/liability by transfer stage (state-dependent) |

Why this structure works under 280E:

It forces an explicit boundary between (a) inventoriable costs for producers under the inventory regulations and (b) normal operating expenses that 280E blocks at the federal level for plant-touching activity.

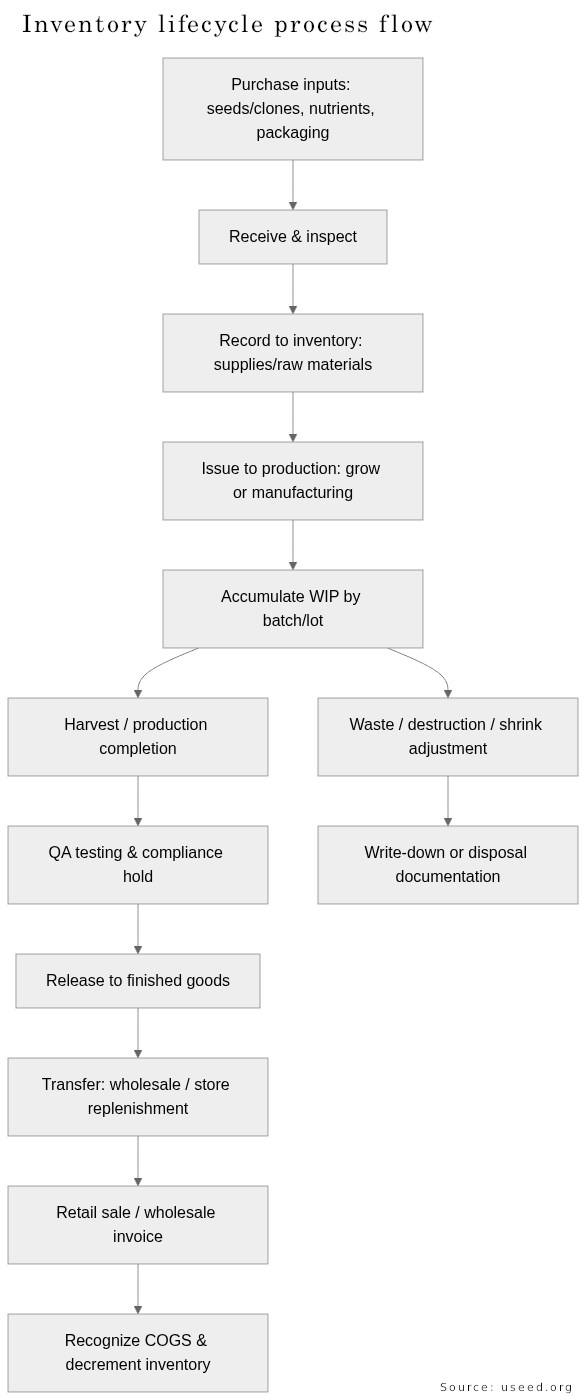

Inventory and cost accounting methods in cannabis

Cost flow assumptions (FIFO/LIFO/weighted average)

Your cost flow method affects gross margin timing and inventory valuation. Whatever method you choose, consistency matters, and you need system support (POS + inventory). Inventory rules and “at cost” concepts in tax start with core inventory principles and regulations.

Cannabis-specific costing concepts worth implementing

- Plant-level costing (cultivation): capture costs by room, strain/batch, and stage (clone/veg/flower/harvest/cure).

- Harvest accounting: treat harvest as the cost-object transition from biological growth cycle to a measurable inventory lot; document yield and waste with sign-offs.

- Shrinkage and waste: keep separate buckets for (a) normal shrink, (b) obsolescence/expired, (c) regulatory destruction. This is necessary for credible inventory valuation and for state reporting in many markets.

Inventory lifecycle process flow (figure)

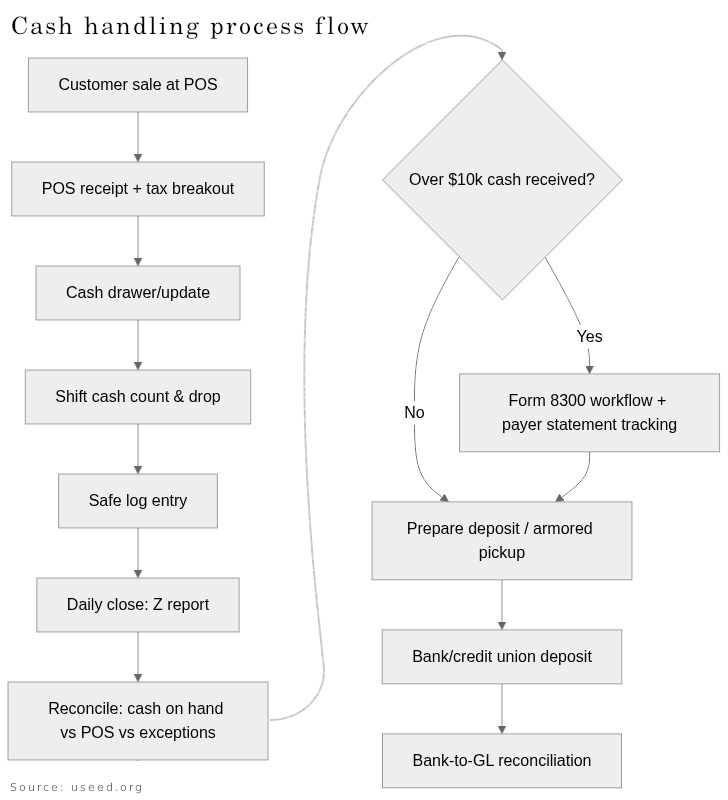

Internal controls and cash management under banking limitations

Banking friction is a policy reality: FinCEN guidance explains how financial institutions can serve marijuana-related businesses while meeting Bank Secrecy Act obligations (customer due diligence, SAR expectations, etc.).

Even when you do have banking, cannabis often remains cash-heavy—so internal controls need to be unusually tight.

Minimum viable cash-control design:

- Dual custody counts: opening, shift drop, close.

- Daily POS “Z” report tied to cash count, card settlement reports, and deposit logs.

- Variance thresholds and documented investigation steps.

- Form 8300 triggers built into the cash receipts workflow (not left to memory). IRS guidance is explicit about filing timelines and payer statements.

- Recordkeeping discipline: the IRS expects books and records that clearly show income/expenses; keep supporting documents for purchases, sales, and payroll.

Cash handling process flow (figure)

Payroll and employment tax operations

Run payroll like a normal regulated employer, because you are one. IRS guidance for employers addresses FICA tax rates, wage base, and payroll reporting mechanics; deposit schedules (monthly vs semiweekly) must be followed.

Cannabis-specific operational risk: cash wages or “off-book” pay creates catastrophic exposure across payroll tax, labor law, and licensing compliance.

Intercompany transactions and transfer pricing for cannabis

Intercompany issues show up in two main ways:

- Tax and consolidation accounting: eliminate intercompany revenue/COGS in consolidated financials, but still track legal-entity profitability for state reporting and licensing.

- Excise-tax valuation of transfers: Some states set excise bases using market proxies for affiliated transfers.

Examples of why this matters:

- Colorado’s retail marijuana excise tax is based on Average Market Rate or contract price. This is explicitly described in Colorado DOR guidance and can affect vertically integrated transfers.

- Nevada reports wholesale cannabis excise tax at a 15% rate and retail excise at 10% for adult-use; statutory and reporting references point to NRS 372A.290.

Practical control: define “transfer order → invoice → excise basis → inventory cost basis” rules in writing, and reconcile them monthly.

Systems recommendations, templates, journal entries, and close checklists

Software options table

This is a short list that covers the core stack layers: accounting GL, POS, and compliance/integration touchpoints. Pricing changes frequently; treat this as directional and confirm current terms at time of purchase.

| Layer | Tool | Best fit | Features | Link |

|---|---|---|---|---|

| Accounting (GL) | Intuit QuickBooks Online | Small to mid-size, multi-location with add-ons | Strong ecosystem; common lender familiarity; pricing varies by plan/country | Official pricing page |

| Accounting (GL) | Xero | Small to mid-size, especially if you want lean workflows | Clear plan tiers; strong bank-feed model where banking supports it | Official pricing page |

| Dispensary POS | Flowhub | Retail operators needing compliance + scaling | POS + ecommerce + payments messaging; highlights long-running compliance integrations | Official homepage |

| Dispensary POS | Dutchie | Retail operators with e-commerce focus | POS tooling includes pricing tiers and tax breakout views (implementation detail matters for accounting mapping) | Official homepage |

Seed-to-sale note:

In many states, seed-to-sale is state-mandated (you don’t pick freely). Your selection task is often “pick systems that integrate cleanly with the state track-and-trace + your POS + your GL,” not “pick a track-and-trace.” This is why POS/vendor integration maturity matters (and why auditors ask for seed-to-sale → inventory → revenue reconciliation evidence).

Sample financial statement templates

These are templates (structure), not GAAP disclosures.

Statement of operations template (simplified)

Net revenue Gross sales Less: discounts/price adjustments Less: returns/allowances Net revenue Cost of goods sold COGS - cannabis products COGS - non-cannabis merchandise Gross profit Operating expenses Payroll - retail/store Payroll - admin Rent Utilities Security & compliance Marketing Depreciation & amortization Professional fees Other operating expenses Total operating expenses Operating income (loss) Other income (expense) Income tax expense (benefit) Net income (loss)

Balance sheet template (simplified)

Assets

Cash and cash equivalents

Accounts receivable

Inventory

Raw materials & packaging

WIP / plants-in-progress

Finished goods

Prepaids and other current assets

Property and equipment, net

Intangible assets (licenses, if applicable), net

Total assets

Liabilities

Accounts payable

Accrued payroll and benefits

Sales tax payable

Excise tax payable

Other accrued liabilities

Debt

Total liabilities

Equity

Common equity

Retained earnings

Total equity

Why templates need cannabis-specific lines:

You want taxes payable split (sales vs cannabis excise vs other) and inventory split by stage. Those splits are essential for both state compliance and federal COGS support.

Journal entry examples

Retail sale with excise and sales taxes (adapt to your state’s tax structure)

Dr Cash / A/R XXX Cr Net revenue YYY Cr Excise tax payable ZZ Cr Sales tax payable AA

Inventory purchase (reseller)

Dr Inventory - finished goods XXX Cr Accounts payable / Cash XXX

COGS recognition at sale

Dr Cost of goods sold XXX Cr Inventory - finished goods XXX

Recorded inventory write-down (expiring product / NRV)

Dr Inventory write-down expense XXX Cr Inventory XXX

Tax workpaper adjustment concept (not a GAAP JE)

For federal returns you typically add back 280E-disallowed expenses in the tax computation; you don’t retroactively delete the expenses from GAAP books. The legal basis is the statute’s denial of deductions/credits.

Month-end close checklist

Keep month-end close short, repeatable, and defensible.

Revenue and cash

- Reconcile POS sales to daily Z reports and to deposits/settlement reports; investigate variances.

- Review discounting, voids, returns, and manual price overrides for policy compliance.

- Review Form 8300 triggers for the month and confirm filings/timelines.

Inventory and COGS

- Reconcile seed-to-sale inventory to GL inventory by category (WIP/FG/accessories).

- Review shrink/waste/destruction logs; ensure approvals and required state documentation are attached.

- Update standard cost / weighted average (if used) and validate cost pools and allocations for producers.

Taxes

- Accrue and reconcile cannabis excise taxes and sales taxes to filed returns (or to filing schedules).

- Validate state-specific tax bases (e.g., NY distributor/retailer taxes; CO AMR excise; CA excise rate effective date).

Payroll

- Reconcile payroll registers to GL; fund payroll taxes per deposit schedule; review any late/penalty notices.

Year-end close checklist

Tax and compliance

- Finalize 280E workpapers: COGS support (by entity/activity) and disallowed expense roll-forward.

- Confirm state decoupling modifications and supporting schedules by jurisdiction (especially where the statute requires specific addback/subtraction reporting).

- 1099/W-2 readiness; confirm payroll tax filings; reconcile year-end payroll liabilities.

Financial reporting

- Perform and document physical inventory counts; ensure cutoff testing (receiving/shipping around year-end).

- Review inventory valuation and NRV write-downs; document assumptions.

- Prepare ASC 606 revenue disclosures and key judgments documentation (pricing variability, returns/allowances).

Audit readiness binder (what auditors and tax examiners actually ask for)

- Inventory policy + allocation drivers, consistently applied.

- Seed-to-sale reports supporting inventory quantities and movement.

- POS reports supporting revenue completeness and tax collection.

- Cash logs, deposit slips, and Form 8300 documentation.

- License documentation and state compliance filings.

Common tax planning strategies and the risk map

Strategies that are generally legitimate (when documented)

- Maximize allowable COGS by doing costing correctly, not aggressively: producers should implement proper absorption costing consistent with inventory regulations; resellers should use correct purchased-goods cost rules.

- Operationalize documentation: timekeeping by function, BOMs, yield reports, destruction logs—these are not “nice-to-haves” under 280E audit risk.

- Multi-entity structuring only where there is a real, separable non-trafficking business with standalone economics; courts have allowed separation in narrow fact patterns (and rejected it when the “other business” is incidental).

Red flags and common failure modes

- Treating retail operating expenses as COGS (especially rent, sales payroll, marketing). The IRS has clearly articulated hostility to “capitalizing around” 280E through §263A mechanics.

- Weak cash controls and missing records (raises both tax and AML-related scrutiny).

- Not tracking state-specific tax bases (AMR/fair market value, potency taxes, local add-ons), leading to incorrect tax accruals and surprise liabilities.

Policy watch: rescheduling and the future of 280E

280E applies only to Schedule I and II trafficking. If marijuana is ultimately moved to Schedule III through final rulemaking, the federal 280E economics could change materially; as of the federal rulemakings cited, DOJ/DEA actions include proposed rescheduling and hearing processes, not a simple overnight tax change.